Here We Go Again...

Don't look now fans, but the S&P 500 is back to within spitting distance of the all-time closing high of 2130.82 set on May 21, 2015. Sure, the bears enjoyed a spirited reversal yesterday afternoon, knocking the Dow back below the 18,000 level and closing at the low of the day. Heck, our friends in fur even managed to push the NASDAQ into negative territory for the day. And to hear the bears tell it, the rally is now over and the sky is about to fall (and yes, there is a bit of sarcasm intended here!).

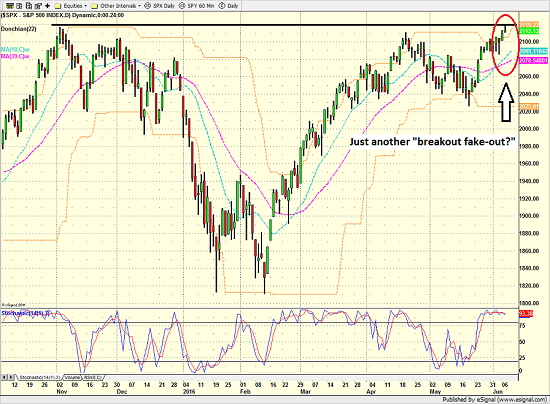

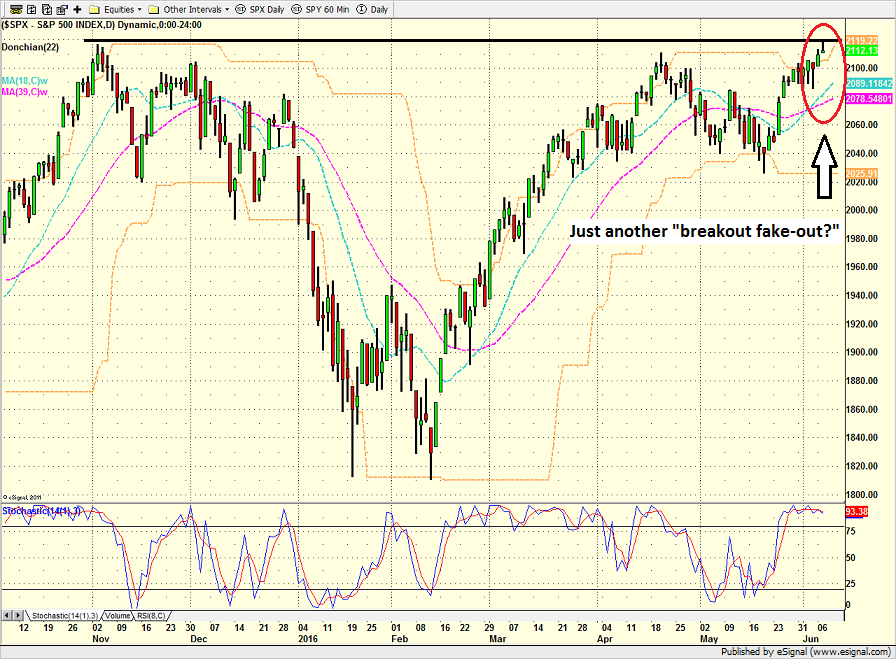

Maybe the pullback will mark the beginning of yet another "breakout fake-out" that has been so prevalent over the past few years. After all, the fact is that all the major indices remain mired in a sideways trading range. A trading range that has been in place for many moons now. But the fact remains that when the opening bell rings at the corner of Broad and Wall, the S&P 500 will be just 18.69 points (0.88%) away from an all-time high.

To be fair though, the current action on the chart below could easily strike some fear into anyone's heart that has recently purchased stocks.

S&P 500 - Daily

View Larger Image

{kind=link}

So, from a very short-term perspective, the bulls would prefer that any pullback be short and shallow. From my perch, I would think that as long as the S&P cash index can stay remain above 2085 the bulls should be given the benefit of the doubt here.

Why the optimism you ask? To be honest, at least part of it has to do with the fact that nobody believes stocks can move higher. The upside is limited, we're told (over and over again). So, anybody with a contrarian bone in their body should be wondering if the crowd just might have it wrong here.

In my humble opinion, the current joyride to the upside is being sponsored by Janet Yellen and her merry band of U.S. central bankers. The latest development in this seemingly never ending saga is the idea that May's jobs report was weak enough to take a June rate hike completely off the table. In fact, Fed Funds futures currently forecast a 0% chance of the Fed Funds Rate being moved up at the June FOMC meeting and just a 24% chance of a hike at the September meeting!

Let's also remember that the Fed doesn't like to hike rates too close to Presidential elections. So in essence, traders see the uber-low rates in the U.S. - and all the associated fancy big-money trades - sticking around for a while longer. And as we've learned over the last few years, easy money trumps all. Oh, and for those keeping score at home, the ECB has embarked on their latest round of bond buying just this morning (this time in the corporate arena). As such, traders may need to remember that asset flows remain the main driver of this game in the short-term.

The question of the day, of course, is if the current attempted jailbreak will become the beginning of a new leg higher in the ongoing bull market - or - the latest in a long string of "breakout fake-outs." So, stick around, this is about to get interesting.

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of Fed Policy

2. The State of U.S. Economic Growth

3. The State of Global Economic Growth

4. The State of the Stock Market Valuations

Thought For The Day:

"When the facts change, I change my mind. What do you do, sir?" — John Maynard Keynes

Here's wishing you green screens and all the best for a great day,

David D. Moenning

Founder: Heritage Capital Research

Chief Investment Officer: Sowell Management Services

Looking for More on the State of the Markets?

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.