The Next Act In The Play...

Good Monday morning and welcome back. To be sure, this week's meeting of Janet Yellen and her merry band of central bankers will be the focal point for the markets. In case you've been sleeping under a rock for the past month, note that the markets are expecting the Fed to raise rates on Wednesday. However, the key will be the statement that accompanies the announcement as well as the updated "dot plot," which details what each FOMC member thinks about the future of interest rates. So while we wait, let's review my key market models and indicators - to make sure we recognize what "is" happening in the market.

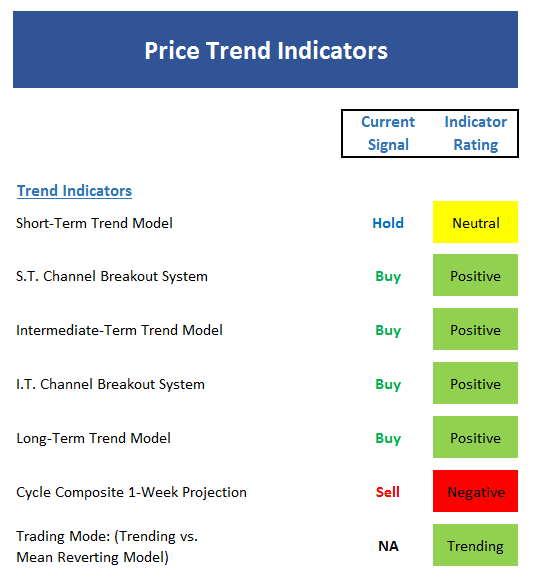

The State of the Trend

We start each week with a look at the "state of the trend" from our objective indicator panel. These indicators are designed to give us a feel for the overall health of the current short- and intermediate-term trend models.

Executive Summary:

- Short-term trend has turned "sloppy" with S&P sitting on 10-day ma, which itself is flat

- There hasn't been enough selling pressure to cause even the S.T. Channel Breakout System to move to sell signal. Although the breakdown point is close at this time.

- The weekly trend and trend model remains strong

- The Intermediate-term Channel Breakout system is in good shape.

- The L.T. Trend Model still solidly positive

- The Cycle Composite now points to stair-step decline into mid-April

- The market remains in a "trending" mode

- Takeaway: We are seeing a pullback within a strong uptrend

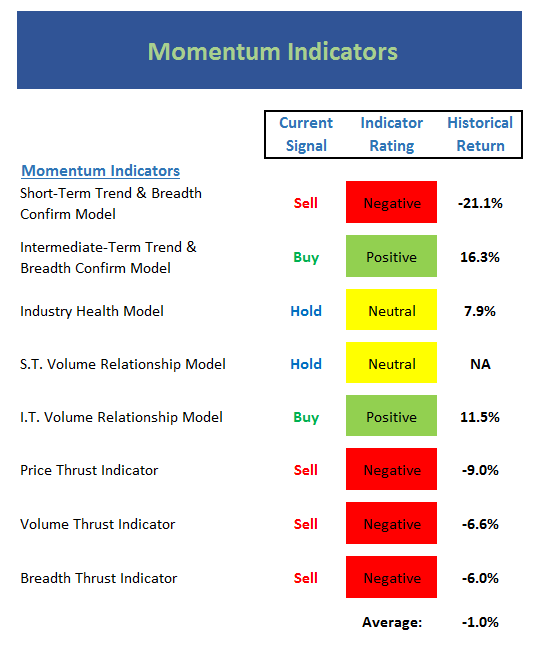

The State of Internal Momentum

Now we turn to the momentum indicators...

Executive Summary:

- The sell signal from the short-term Trend & Breadth Confirm model is a sign of underlying weakness

- However, the intermediate-term model reading is still strong

- The reading of the Industry Health model is still decent, but the direction of the indicator is now down slightly.

- Demand volume and supply volume are equal at this time. It is worth noting that demand volume has been much weaker on most recent rally than it was during the November-December move.

- The reading of the intermediate-term Volume Relationship model is still in good shape, but demand and supply volume lines are both heading in wrong direction for bulls.

- The Price Thrust indicators (which uses the NASDAQ composite) turned negative this week

- Both the Volume and Breadth Thrust indicators are also negative here

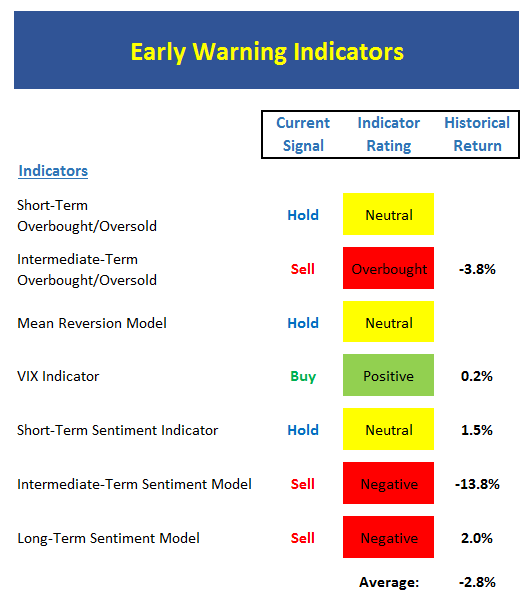

The State of the "Trade"

Next up is the "early warning" board, which is designed to indicate when traders may start to "go the other way" -- for a trade.

Executive Summary:

- The short-term Overbought condition has been worked off with indicators now approaching oversold

- The intermediate- and long-term situation is just the opposite - still overbought

- The low volatility environment has made it difficult for the Mean Reversion model to flash a signal in either direction

- Both the short- and intermediate-term VIX models appear confused (also likely due to the extended low vol environment)

- The extreme reading from short-term sentiment model has been worked off

- Sentiment readings remain extremely negative from both short- and intermediate-term perspective

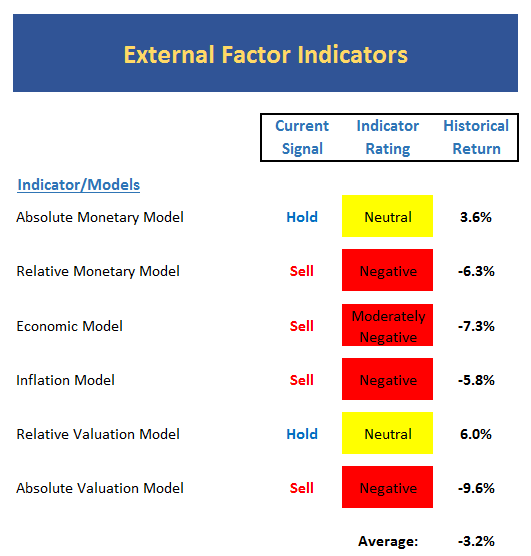

The State of the Macro Picture

Now let's move on to the market's "external factors" - the indicators designed to tell us the state of the big-picture market drivers including monetary conditions, the economy, inflation, and valuations.

Executive Summary:

- There is no change to the monetary models. However, with the Fed poised to raise rates and yields about threatening to break to new highs for the cycle, the monetary environment remains negative.

- To review, the Economic Model appears to have given a false signal and as such, should be ignored at this stage

- The Inflation Model reading has now moved up into the "Strong Inflation Pressures" zone

- Relative Valuations - once a friend to the bulls - are now neutral and moving in the wrong direction

- Absolute Valuation Model remains negative

- The Median P/E Valuation Model (not shown) has reached the highest level seen since the technology bubble burst

- Bottom Line: Valuations will become a problem if a new crisis develops or the premise for rally falters

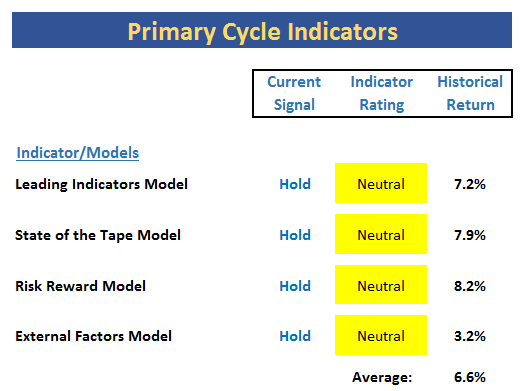

The State of the Big-Picture Market Models

Finally, let's review our favorite big-picture market models, which are designed to tell us which team is in control of the prevailing major trend.

Executive Summary:

- The color on the board says it all

- The Leading Indicators Model is back to neutral zone - albeit by the skinniest of margins

- The State of the Tape Model suggests the broad market is not as healthy as level of the S&P 500 might suggest

- The Risk/Reward Model remains burdened by the monetary and sentiment readings

- The External Factors Model is too close to negative for my comfort - probably most disconcerting indicator in the bunch this week

The Takeaway...

My take on the overall status of the indicators is that a corrective phase is either underway or the likely next act in this play. However, given the backdrop and the improving economic picture, I would expect to see a garden variety pullback in the 3-5% zone. And unless something changes along the way, it would make sense to be ready to "buy the dip" in anticipation of the late-spring/summer rally projected by our cycle work. Yet at the same time, let's be clear that this is NOT a low-risk environment.

Thought For The Day:

To wish you were someone else is to waste the person you are -Sven Goran Eriksson

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of the Fed's Next Move (After Wednesday)

2. The State of Trump Administration Policies

3. The State of the U.S. Economy

4. The State of Global Central Bank Policies (Think ECB pulling back on QE)

Wishing you green screens and all the best for a great day,

David D. Moenning

Chief Investment Officer

Sowell Management Services

Looking for a "Modern" approach to Asset Allocation and Portfolio Design?

Looking for More on the State of the Markets?

Investment Pros: Looking to modernize your asset allocations, add risk management to client portfolios, or outsource portfolio Management? Contact Eric@SowellManagement.com

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.