Window "Undressing" May Be At Work

The headlines blared that stocks soared Wednesday in response to improvements in the trade war. Apparently, China was making noise about a new policy designed to increase access to the country's economy for foreign companies. Diving into the story, it certainly sounded like things were moving in the right direction. As such, stocks opened strong and rallied throughout the morning. By lunchtime, it felt like the tide might be turning and maybe, just maybe, Santa might make an appearance after all.

However, as has been the case lately, the improved mood didn't last too terribly long. Sellers and their computers hit the tape hard at around 1:15 pm EST and as you can see on the 1-min chart of the S&P 500 below, the index quickly gave up more than 1% and then wound up sinking into the close, finishing at the low of the day.

S&P 500 - Daily

View Larger Chart

{kind=link}

As the closing bell rang, one of my colleagues pinged me. His message was short and to the point. He called the action, "Horrid, one of the worst tapes I've seen in a long time." I guess finishing 300 points off the high - again - will do that.

The bottom line is that any/all rallies are being sold into lately. This means that in addition to the scary down days investors have to deal with, even the good days quickly come under attack.

So what gives? Why all the selling? Why aren't stocks rebounding the way they "normally" do after a big decline?

Window Dressing Cuts Both Ways

Anyone who has been in the stock market game for a while knows about the practice of "window dressing." While technically illegal, the idea is that managers tend to bid up the prices of their biggest holdings at the end of reporting periods (think fiscal year-ends, quarters, and calendar years). The idea is to "dress up" your portfolio for the report you're going to write to investors.

However, this concept can go both ways, especially when there is a perceived shift in the market environment. And make no mistake about it; there is definitely a change happening in the current market.

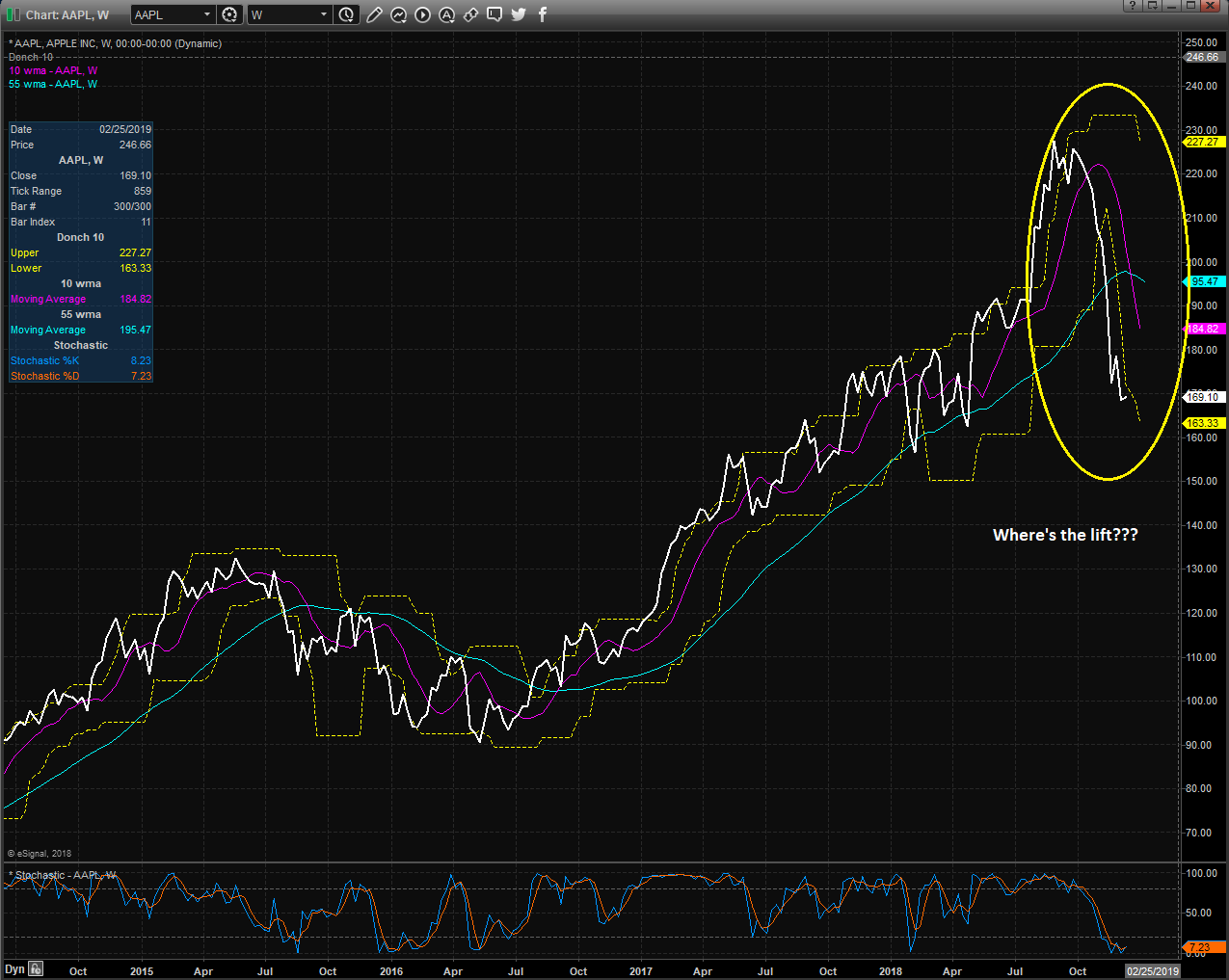

Exhibit A in my argument here is the action in most of the "FAANGs." Take a peek at a weekly chart of Facebook (FB), Apple (AAPL), Netflix (NFLX), and Google parent, Alphabet (GOOGL) and you'll see what I mean. As an example, here's a chart of Apple.

Apple (AAPL) - Weekly

View Larger Chart

{kind=link}

These former market darlings have been hit and hit hard during the current corrective phase. Granted, some of these names had been overdone to the upside and valuations had become extreme. However, it is important to keep in mind that this group had been the market's leaders - for a LONG time.

In short, the so-called "FAANG+ Trade" wound up becoming VERY crowded as everyone on the planet knew that the key to outperforming the market was to own a big slug of the FAANGs.

But as the saying goes, all good things come to an end. Yes, even in the stock market. Thus, many analysts argue that the FAANG+ trade is being "unwound" in front of our eyes here. This explains why we aren't seeing a rush back into these highfliers.

So, instead of managers "dressing up" their portfolio by adding shares of FB, AAPL, NFLX, and/or GOOGL, perhaps it's the other way around. Maybe, managers are looking to reduce their exposure to these names in order to right-size the positions.

If this is the case, then what we are seeing is window "undressing." And it could go on for a while.

Or not...

Call me cynical if you must, but I've been at this game a very long time (I entered the business in 1980 and began managing people's money for a living 31 years ago in 1987). And one of the things I've learned is that the S&P 500 doesn't finish calendar years in the red very often.

Don't look now fans, but as of yesterday's close, the year-to-date return for the S&P 500 index stands at -0.83%. And with dividends reinvested, the venerable blue chip index is up +1%. Thus, I'm of the mind that it wouldn't take much to push the index back into the black for the year. You know, so that everyone can go home happy.

But until/unless Santa can deliver some green on the screens to finish the year, I'm going to opine that the action has indeed been rough lately, that all rallies are being sold, and that we may be seeing a rare case of "window undressing" here. Time will tell.

Thought For The Day:

Honesty is the best policy. If I lose mine honor, I lose myself. -Shakespeare

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

HCR Focuses on a Risk-Managed Approach to Investing

What Risk Management Can and Cannot Do

HCR Awarded Top Honors in 2018 NAAIM Shark Tank Portfolio Strategy Competition

Each year, NAAIM (National Association of Active Investment Managers) hosts a competition to identify the best actively managed investment strategies. In April, HCR's Dave Moenning took home first place for his flagship risk management strategy.

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: GOOGL - Note that positions may change at any time.

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.