A New Leg Higher? Or...

I'd like to start this week's missive by wishing everyone a Happy Veterans Day and hoping that we can all take at least a moment to say a silent thank you to those who have kept our country safe for more than 240 years.

Banks and the bond market have the good sense to be closed today, while the stock exchanges are open during this holiday. A fact I discovered many years ago when I awoke late one Veteran's Day morning, turned on my computer, and wondered why my screens were blinking!

I am going to try and keep this brief as I've got a plane to catch. I'm heading to Dallas for NAAIM's Outlook Conference Monday and Tuesday, where I'm hosting the NAAIM Shark Tank Investing Strategy Competition. I think we have a great lineup of competitors and the event should be fun.

A New Bull Leg?

Looking at the stock market, the question of the day - at least in my mind - is if we are seeing the beginning of a fresh leg in an ongoing cyclical and secular bull move -or- the setup for yet another "breakout fakeout."

Let's Review

If you will recall, since January 2018, the stock market has made a series of new all-time highs. First there was the September 20, 2018 high, which was followed by a brief breakout flirtation and then a brutal decline of -19.8% as the world fretted about trade and a Fed overshoot.

Next came the Fed flip-flop, which produced a furious recovery. This move wound up pushing the S&P 500 to a new high on April 30, 2019. But, less than a week later, the market became obsessed with recession fears and the S&P fell -6.8% in a month.

As it became clear that the U.S. consumer hadn't wavered from its job-induced good mood, the market once again looked ahead to better days and hit a fresh new high on July 28, 2019. What followed, as you might suspect, was an almost immediate reversal, which took the S&P down -6.1% within three short weeks of the most recent high-water mark.

From there, stocks once again recovered and by early September were knocking on the door of new highs again. However, yet another tweet/trade-induced pullback occurred - this time pushing stocks down -4% in short order.

Have Things Changed?

But then it happened (well, I "think" it happened, anyway). Apparently, investors took notice of the facts that the global economic data had stopped going down, that Global Central Bankers were on the case, and that the U.S. economy was still muddling along and nowhere near recession.

From my seat, the bottom line thinking appeared to be that the trade war wasn't likely to get worse, lower rates were starting to work their magic on the economy, and U.S. consumers, while perhaps a bit concerned about the drama in D.C., appeared to remain in their happy place from a spending perspective.

The end result has been a steady climb for the S&P and NASDAQ indices over the last thirteen months. While the advance may best be described as painstaking, the good news is that we have seen a series of "higher highs and higher lows" along the way.

The Question At Hand

Yet, today's review of how we got here doesn't really address the question at hand. So here goes.

My take is that the most recent break for the border "looks and feels" better than those in the past. First, stocks appear to be ignoring the back-and-forth in trade negotiations. For example, while good news did create some enthusiasm last week, the market basically yawned when the White House "walked back" the hope that tariffs would be rolled back as part of the "Phase One" deal.

In addition, this time around, it isn't just the big tech leaders doing the heavy lifting. Don't look now fans, but those cyclical names are participating in the fun here. Industrials have stepped lively to a new all-time high. The left-for-dead health care sector is within a stone's throw of a new high. Heck, even the much-maligned financials are movin' on up. And with the NYSE A/D line hitting fresh new highs, it is hard to argue that the action should be viewed as bearish.

History Suggests Siding With The Bulls

Next, I've seen several reports detailing the historical positives of what transpires at the end of calendar years when the S&P has been up more than 20% at the end of October. If memory serves, history shows that the S&P 500 has advanced into the end of the year by an average of more than 5%. As such, a little something called "performance anxiety" by portfolio managers with cash on the sidelines may be creeping in here.

Yet at the same time, we MUST recognize that stocks are now overbought, and that sentiment is becoming overly upbeat. As such, a pullback would seem to be the next logical move. History supports this idea as the reports on what happens when stocks are up 20% through October also show that the S&P has moved below where it stood on October 31st on five of the seven occurrences.

So, while history suggests that this might be a good time to stay seated on the bull train, there also appears to be hope for anyone looking to "buy the dip" before the holiday spirit takes over Wall Street.

Since it's the start of a new week, it's now time to put aside my subjective view of the action and to review the "state" of our indicator boards.

Have a great week!

Weekly Market Model Review

Each week we do a disciplined, deep dive into our key market indicators and models. The overall goal of this exercise is to (a) remove emotion from the investment process, (b) stay "in tune" with the primary market cycles, and (c) remain cognizant of the risk/reward environment.

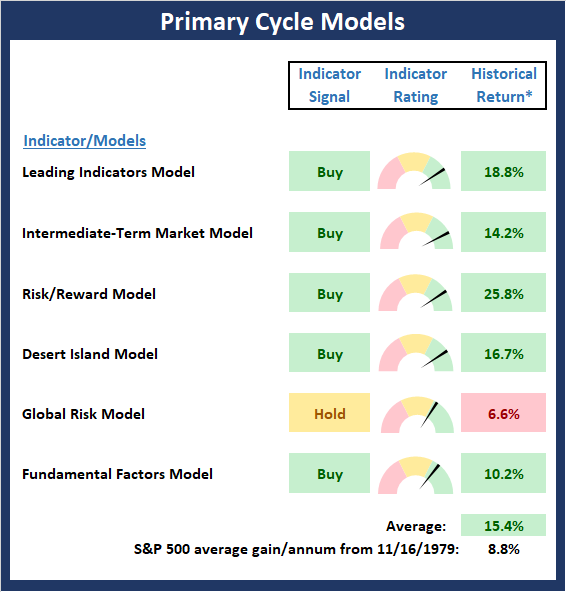

The Major Market Models

We start with six of our favorite long-term market models. These models are designed to help determine the "state" of the overall market.

There were no obvious changes to the Primary Cycle board this week. However, there was some nuanced improvement to report as my Fundamental Factors model that focuses on monetary conditions, the economy, earnings, inflation and valuation upticked in terms of the hypothetical average historical return based on the current readings of the indicators. The net result produces a hypothetical average return over 15%, which is well above the average since 1980 of 8.8%.

This week's mean percentage score of my 6 favorite market models improved to 76.7% from 75.6% last week while the median held steady at 80.0%.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View My Favorite Market Models Online

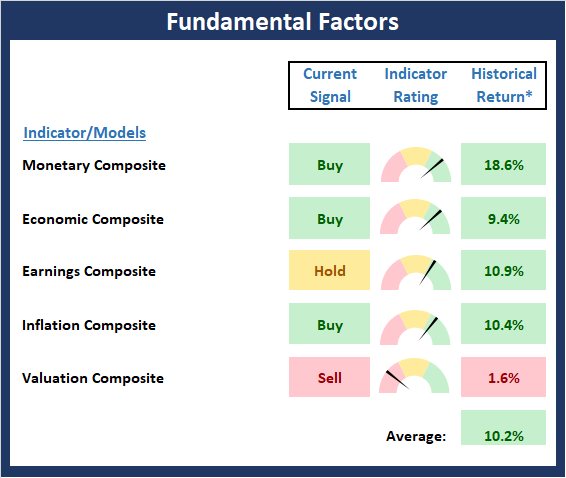

The State of the Fundamental Backdrop

Next, we review the market's fundamental factors in the areas of interest rates, the economy, inflation, and valuations.

There was one change to the Fundamental Factor board this week. One of the components of the Earnings Composite upticked from negative to neutral. While this didn't change the overall reading of the Earnings Composite model, it did boost the historical return from 2.3% to 10.9%, which, in my book, is worth noting. Overall, as I've been saying, I believe the Fundamentals continue to support an offensive stance in portfolios.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Fundamental Indicator Board Online

{kind=link}

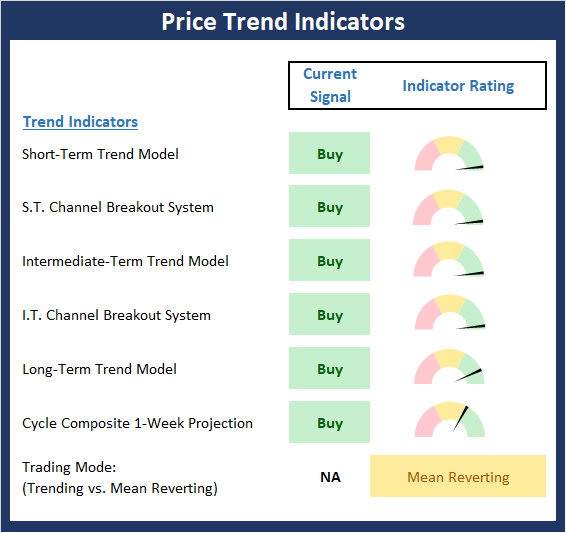

The State of the Trend

From there, we look at the state of the current trend. This board of indicators is designed to tell us about the overall technical health of the current trend.

The Price Trend board continues to sport an awful lot of green boxes. The lone holdout continues to be the Trading Mode model, which is comprised of five indicators designed to determine whether stocks are in a trending or mean reverting environment. To date, the model has been reluctant to call the current environment a trending market. However, if the breakout to new highs is confirmed by other indices, we should expect this model to turn green at some point soon.

NOT INDIVIDUAL INVESTMENT ADVICE.

View Trend Indicator Board Online

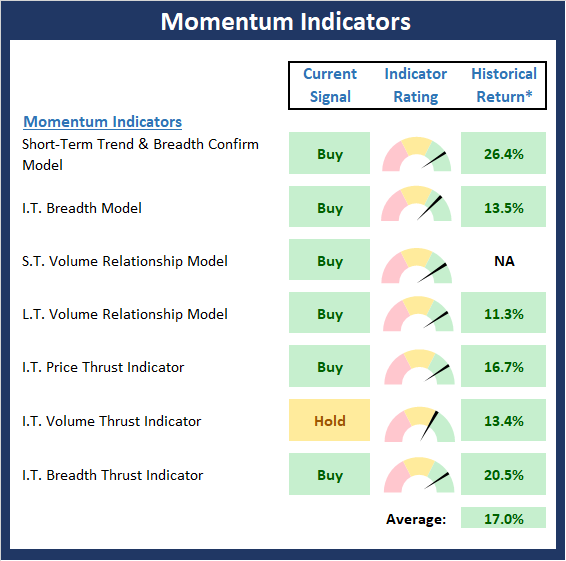

The State of Internal Momentum

Next, we analyze the "oomph" behind the current trend via our group of market momentum indicators/models.

The Momentum board remains in good shape with only the Volume Thrust indicator not sporting a buy signal. Given that this is an intermediate-term indicator, this too is likely to turn green if the current rally holds. But my bottom line takeaway is that this market has enough positive momentum to sustain the bulls for a while from a big picture point of view.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Momentum Indicator Board Online

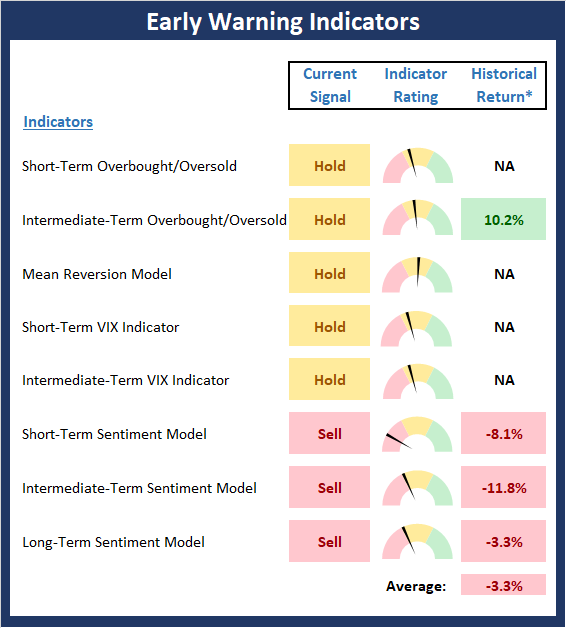

Early Warning Signals

Once we have identified the current environment, the state of the trend, and the degree of momentum behind the move, we review the potential for a counter-trend move to begin. This batch of indicators is designed to suggest when the table is set for the trend to "go the other way."

The message from the Early Warning board is now clear. Although I can argue we may be witnessing a "good overbought" condition (where the market gets overbought and stays overbought while it trends steadily higher), the board suggests that the table is now set for a counter-trend move. However, it is important to keep in mind that such moves generally need a "trigger" to get things going the other way. And with the number of trading days left in the year starting to grow thin, I expect the current trend to continue until/unless a bearish "trigger" presents itself and causes traders to rethink the current theme.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Early Warning Indicator Board Online

Thought For The Day:

It requires less character to discover the faults of others, than to tolerate them. -J. Petit Senn

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: None - Note that positions may change at any time.

Leading Indicators Model: A group of indicators that have historically shown tendencies to lead the market at major turning points.

Intermediate-Term Market Model: A composite model (model of models) focused on trend and momentum indicators which has been designed to provide identify intermediate-term trading opportunities.

Risk/Reward Model: A model-of-models intended to provide an overall view of the state of the risk/reward environment. The model includes tape, monetary, and sentiment indicators as well as 7 big-picture market model readings.

Desert Island Model: If I was stranded on a desert island with access to only one market model to manage money with, this would be the model. The model is a comprehensive model-of-models comprised of trend, momentum, mean reversion, economic, monetary, sentiment, and factor-based indicators/models.

External Factors Model: A model-of-models designed to provide a reading on the "macro state" of the market environment. The model is comprised of indicators/models in the areas of various index yields, industrial production, investors sentiment, and historic volatility.

Short-Term Trend-and-Breadth Signal Explained: History shows the most reliable market moves tend to occur when the breadth indices are in gear with the major market averages. When the breadth measures diverge, investors should take note that a trend reversal may be at hand. This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 5-day smoothing and the All-Cap Equal Weighted Equity Series is above its 25-day smoothing, the equity index has gained at a rate of +32.5% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +13.3% per year. And when both are below, the equity index has lost +23.6% per year.

Channel Breakout System Explained: The short-term and intermediate-term Channel Breakout Systems are modified versions of the Donchian Channel indicator. According to Wikipedia, "The Donchian channel is an indicator used in market trading developed by Richard Donchian. It is formed by taking the highest high and the lowest low of the last n periods. The area between the high and the low is the channel for the period chosen."

Intermediate-Term Trend-and-Breadth Signal Explained: This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 45-day smoothing and the All-Cap Equal Weighted Equity Series is above its 45-day smoothing, the equity index has gained at a rate of +17.6% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +6.5% per year. And when both are below, the equity index has lost -1.3% per year.

Cycle Composite Projections: The cycle composite combines the 1-year Seasonal, 4-year Presidential, and 10-year Decennial cycles. The indicator reading shown uses the cycle projection for the upcoming week.

Trading Mode Indicator: This indicator attempts to identify whether the current trading environment is "trending" or "mean reverting." The indicator takes the composite reading of the Efficiency Ratio, the Average Correlation Coefficient, and Trend Strength models.

Volume Relationship Models: These models review the relationship between "supply" and "demand" volume over the short- and intermediate-term time frames.

Price Thrust Model Explained: This indicator measures the 3-day rate of change of the Value Line Composite relative to the standard deviation of the 30-day average. When the Value Line's 3-day rate of change have moved above 0.5 standard deviation of the 30-day average ROC, a "thrust" occurs and since 2000, the Value Line Composite has gained ground at a rate of +20.6% per year. When the indicator is below 0.5 standard deviation of the 30-day, the Value Line has lost ground at a rate of -10.0% per year. And when neutral, the Value Line has gained at a rate of +5.9% per year.

Volume Thrust Model Explained: This indicator uses NASDAQ volume data to indicate bullish and bearish conditions for the NASDAQ Composite Index. The indicator plots the ratio of the 10-day total of NASDAQ daily advancing volume (i.e., the total volume traded in stocks which rose in price each day) to the 10-day total of daily declining volume (volume traded in stocks which fell each day). This ratio indicates when advancing stocks are attracting the majority of the volume (readings above 1.0) and when declining stocks are seeing the heaviest trading (readings below 1.0). This indicator thus supports the case that a rising market supported by heavier volume in the advancing issues tends to be the most bullish condition, while a declining market with downside volume dominating confirms bearish conditions. When in a positive mode, the NASDAQ Composite has gained at a rate of +38.3% per year, When neutral, the NASDAQ has gained at a rate of +13.3% per year. And when negative, the NASDAQ has lost at a rate of -14.279% per year.

Breadth Thrust Model Explained: This indicator uses the number of NASDAQ-listed stocks advancing and declining to indicate bullish or bearish breadth conditions for the NASDAQ Composite. The indicator plots the ratio of the 10-day total of the number of stocks rising on the NASDAQ each day to the 10-day total of the number of stocks declining each day. Using 10-day totals smooths the random daily fluctuations and gives indications on an intermediate-term basis. As expected, the NASDAQ Composite performs much better when the 10-day A/D ratio is high (strong breadth) and worse when the indicator is in its lower mode (weak breadth). The most bullish conditions for the NASDAQ when the 10-day A/D indicator is not only high, but has recently posted an extreme high reading and thus indicated a thrust of upside momentum. Bearish conditions are confirmed when the indicator is low and has recently signaled a downside breadth thrust. In positive mode, the NASDAQ has gained at a rate of +22.1% per year since 1981. In a neutral mode, the NASDAQ has gained at a rate of +14.5% per year. And when in a negative mode, the NASDAQ has lost at a rate of -6.4% per year.

Short-Term Overbought/sold Indicator: This indicator is the current reading of the 14,1,3 stochastic oscillator. When the oscillator is above 80 and the %K is above the %D, the indicator gives an overbought reading. Conversely, when the oscillator is below 20 and %K is below its %D, the indicator is oversold.

Intermediate-Term Overbought/sold Indicator: This indicator is a 40-day RSI reading. When above 57.5, the indicator is considered overbought and wnen below 45 it is oversold.

Mean Reversion Model: This is a diffusion model consisting of five indicators that can produce buy and sell signals based on overbought/sold conditions.

VIX Indicator: This indicators looks at the current reading of the VIX relative to standard deviation bands. When the indicator reaches an extreme reading in either direction, it is an indication that a market trend could reverse in the near-term.

Short-Term Sentiment Indicator: This is a model-of-models composed of 18 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a short-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Intermediate-Term Sentiment Indicator: This is a model-of-models composed of 7 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a intermediate-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Long-Term Sentiment Indicator: This is a model-of-models composed of 6 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a long-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Absolute Monetary Model Explained: The popular cliche, "Don't fight the Fed" is really a testament to the profound impact that interest rates and Fed policy have on the market. It is a proven fact that monetary conditions are one of the most powerful influences on the direction of stock prices. The Absolute Monetary Model looks at the current level of interest rates relative to historical levels and Fed policy.

Relative Monetary Model Explained: The "relative" monetary model looks at monetary indicators relative to recent levels as well as rates of change and Fed Policy.

Economic Model Explained: During the middle of bull and bear markets, understanding the overall health of the economy and how it impacts the stock market is one of the few truly logical aspects of the stock market. When our Economic model sports a "positive" reading, history (beginning in 1965) shows that stocks enjoy returns in excess of 21% per year. Yet, when the model's reading falls into the "negative" zone, the S&P has lost nearly -25% per year. However, it is vital to understand that there are times when good economic news is actually bad for stocks and vice versa. Thus, the Economic model can help investors stay in tune with where we are in the overall economic cycle.

Inflation Model Explained: They say that "the tape tells all." However, one of the best "big picture" indicators of what the market is expected to do next is inflation. Simply put, since 1962, when the model indicates that inflationary pressures are strong, stocks have lost ground. Yet, when inflationary pressures are low, the S&P 500 has gained ground at a rate in excess of 13%. The bottom line is inflation is one of the primary drivers of stock market returns.

Valuation Model Explained: If you want to get analysts really riled up, you need only to begin a discussion of market valuation. While the question of whether stocks are overvalued or undervalued appears to be a simple one, the subject is actually extremely complex. To simplify the subject dramatically, investors must first determine if they should focus on relative valuation (which include the current level of interest rates) or absolute valuation measures (the more traditional readings of Price/Earnings, Price/Dividend, and Price/Book Value). We believe that it is important to recognize that environments change. And as such, the market's focus and corresponding view of valuations are likely to change as well. Thus, we depend on our Valuation Models to help us keep our eye on the ball.

Disclosures

NOT INVESTMENT ADVICE. The opinions and forecasts expressed herein are those of Mr. David Moenning and Heritage Capital Research and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning of Heritage Capital Research is an investment adviser representative of Eastsound Capital Advisors, LLC, a registered investment advisor. The adviser may not transact business in states where it is not appropriately registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

Mr. Moenning and Heritage Capital Research may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

The author neither endorses nor warrants the content of this site, any embedded advertisement, or any linked resource. The author or his managed funds may hold either long or short positions in the referenced securities. Republication rights must be expressly granted by author in writing.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.