A Pair of Pivots Worth Watching

The primary purpose of my oftentimes meandering market missive is to identify the primary drivers of the near-term market action. As I've stated a time or twenty, I'm of the mind that if I can understand what markets are doing and why, staying opinion agnostic in the process, I feel I should have a decent chance at keeping portfolios positioned accordingly.

To be sure, there is no shortage of issues for investors to deal with right now. The war. The Fed. Inflation. Growth expectations. The yield curve. Additional geopolitical issues. Supply chain problems. China. And a little thing called COVID. All of which are keeping traders on their toes these days. And it is important to recognize that the market's "narrative" (I.E. the street's explanation of why markets are moving the way they are) can/does shift quickly in this environment.

But perhaps the biggest news last week revolved around the apparent pivots from an unlikely pair: Powell and Putin.

Cutting to the chase, Jay Powell got everyone's attention on March 21st when he said, "We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so."

Bam. In a heartbeat, markets began to price-in the idea that the Fed will "frontload" upcoming rate hikes. Instead of raising rates by 25 basis points at each of the upcoming FOMC meetings, Powell's merry band of central bankers would hike rates by 50 basis points (or more?) at the next couple meetings. And in short, the Fed is letting us all know that they are now in "inflation fighting" mode.

This idea was supported by a flurry of Fedspeak, with multiple Fed officials (Bullard, Mester, and Daly) all talking about 50 basis point moves. And the markets responded, with the yield on the 10-year surging from 2.15% to just a smidge under 2.5% last week.

While it may sound strange, the stock market didn't freak out over the Fed donning their inflation fighter capes. No, it appears that investors see the Fed's shift as a positive since (a) stocks have historically been a strong hedge against inflation, (b) the market has tended to rise during the first year of a tightening cycle, and (c) the economy remains stronger than expected. Which, of course, is a good thing from an earnings perspective.

Next, we should note that stocks appear to be following the historical script for unsettling geopolitical events. Summing up, my take on the history of these things is stocks initially experience a short/sharp selloff on the uncertainty caused by the event. But then the market tends to recover fairly quickly as the focus returns to the economic/macro backdrop. Which, in this case, remains pretty positive.

Speaking of geopolitical events, word out of Russia on Friday suggests that Putin may be making a pivot of his own. As in changing the objective of his unconscionable invasion. Instead of trying to waltz in and take over the entire country while the world watches idly by - a plan that is clearly not going well - on Friday, it sounded like Putin might be looking for a way to "get a win." As in, perhaps "just" taking the eastern sections of Ukraine already occupied by Russian supporting separatists. We shall see.

The good news is the stock market has been movin' on up over the last two weeks and, in the process, has retraced a healthy chunk of the recent decline. As of Friday's close, the S&P 500 is just 5.5% from its all-time highs. Given a war, surging inflation, the Fed's pivot, and a spike in interest rates, I think we can say the market is handling things pretty darn well.

Yes, this is a glass-is-half-full assessment. And we must remember that things can/do change quickly and may not go smoothly going forward. But when looking ahead, the key question for me is if persistent/higher inflation and/or Fed policy will cause economic growth to slow. Because from my seat, it's the outlook growth that matters most to the stock market in the end.

Now let's review the "state of the market" through the lens of our market models...

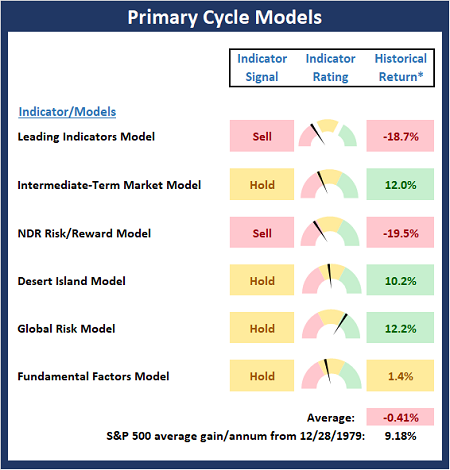

The Big-Picture Market Models

We start with six of our favorite long-term market models. These models are designed to help determine the "state" of the overall market.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR.

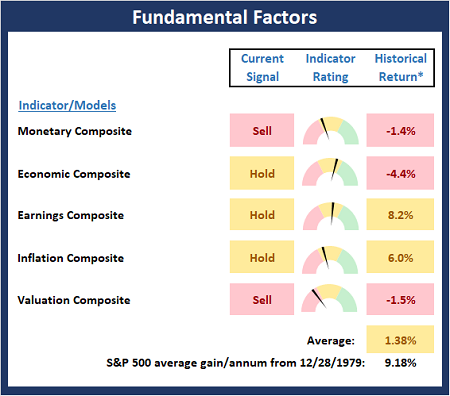

The Fundamental Backdrop

Next, we review the market's fundamental factors including interest rates, the economy, earnings, inflation, and valuations.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR.

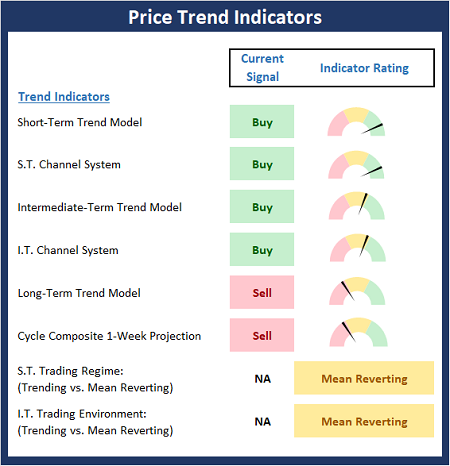

The State of the Trend

After reviewing the big-picture models and the fundamental backdrop, I like to look at the state of the current trend. This board of indicators is designed to tell us about the overall technical health of the market's trend.

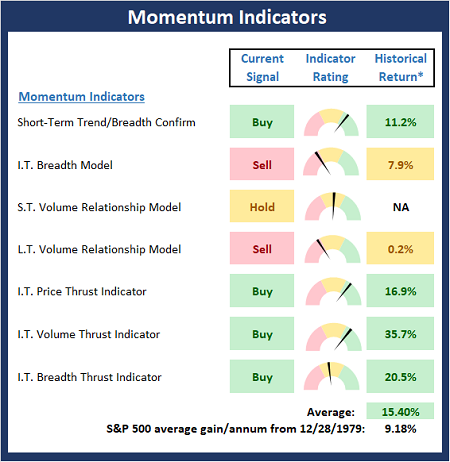

The State of Internal Momentum

Next, we analyze the momentum indicators/models to determine if there is any "oomph" behind the current move.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR.

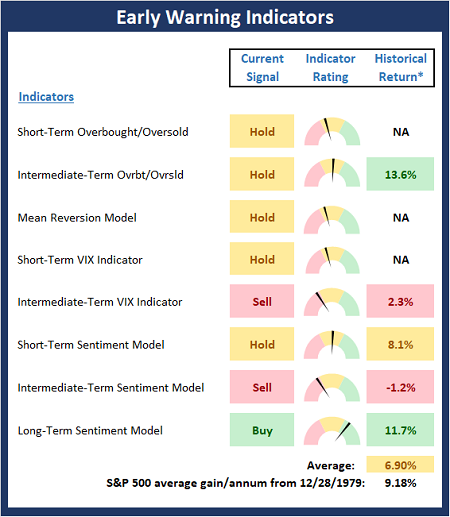

Early Warning Indicators

Finally, we look at our early warning indicators to gauge the potential for countertrend moves. This batch of indicators is designed to suggest when the table is set for the trend to "go the other way."

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR.

Thought for the Day:

Success is simple. Do what's right, the right way, at the right time. -Arnold Glasow

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research, a Registered Investment Advisor

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: None - Note that positions may change at any time.

NOT INDIVIDUAL INVESTMENT ADVICE. IMPORTANT FURTHER DISCLOSURES