Final Thought On Valuations: The Bears Could Be Wrong

I've spent a fair amount time recently talking about the various risks of the current market environment. In short, my view is that risk factors are elevated at this time from a macro perspective. I have suggested that this is due at least in part, to market valuation levels, many of which remain at or near historical extremes.

Yet, we must remember that risk factors alone do not necessarily "cause" bull markets to end or bear markets to begin. No, in my opinion, they either indicate that (a) the probability of a meaningful reversal is high and/or (b) the degree of the ensuing unpleasantry may be increased if the bears are able to find a catalyst to turn the tide.

However, one thing that I've learned over the years is that bull markets tend to last longer than those in the bear camp can possibly imagine. The current grind higher is a perfect example. There are all kinds of problems out there to fret about and yet stocks continue to stair-step their way higher. All the while, our furry friends constantly remind us that stocks are sure to implode at any moment. As such, they say, you need to take precautionary measures - now!

The problem with investing based on one's "view of the world" is that your "view" could wind up being flawed. In other words, you could be wrong. As the late Marty Zweig was famous for saying, "Those who rely on a crystal ball in investing will likely end of with an awful lot of crushed glass in their portfolio."

And on that note, I think we owe it to ourselves to recognize that on the subject of market valuations, the view that stocks are wildly overvalued could very well end up being wrong.

At issue here is the historically low level of interest rates. Sure, rates are up off the all-time lows seen in July of last year. But let's also keep in mind that the yield on the US 10-year is still less than half where it was 10 years ago.

This is important because there isn't much in the way of competition for stocks these days. And while this argument is an oversimplification of a very complex issue, given that central banks continue to pump money into the global financial system on a monthly basis, well, the thing to realize is all that fresh capital has to go somewhere, now doesn't it?

So, with a world that appears to be awash in cash looking for a home, a fair amount of money continues to find its way into the U.S. stock market. From my seat, this helps explain why volatility remains low and any/all dips continue to be bought.

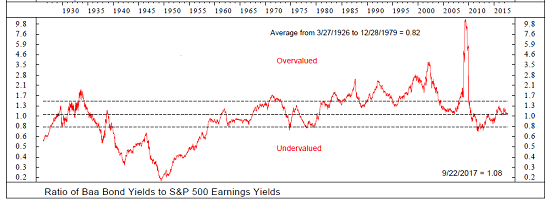

Getting back to the subject of low rates, it is worth recognizing that when viewed through an earnings yield lens (earnings yield = total S&P 500 earnings divided by the index price) stock market valuations are no worse than neutral. Check out the chart below, which goes back into the 1920's.

Using the chart of earnings yield as a guide, one could argue that relative to the levels seen since 1970, stocks are even undervalued.

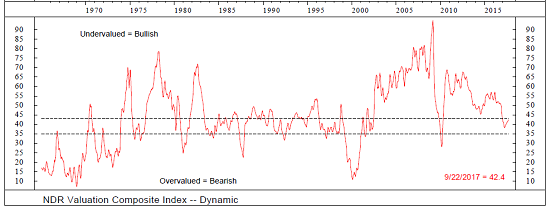

Another way to look at this issue is to compare the various yields against their 10-year historical averages. Ned Davis Research combines things such as Earnings, Dividend, and Book Value yields with the same adjusted for inflation, as well as the spread in these yields and bond yields. When tallied together, you wind up with what NDR calls a "valuation composite."

{kind=link}

{kind=link}

As you can see on the chart above, the current reading of this indicator is neutral. And in fact, the model is just a hair away from the undervalued zone. So, again, one can argue that on a relative basis, stocks are not at all overvalued here.

So Which Is It?

The problem with all of this is the message from the "absolute valuation metrics" (Price-to-Earnings, Dividends, Sales, etc.) is that stock market valuations are sky high and warning of impending doom while the message from the "relative valuation indicators" is, everything is fine and stocks have plenty of room to advance.

From my perch, it's probably a little of both. Stocks ARE indeed overvalued by traditional measures. However, the "yea, but" is with rates so low, there is no competition for stocks.

So... my macro takeaway from this exercise is that as long as (a) earnings continue to improve, (b) inflation expectations remain low, (c) economic growth continues to be decent, and (d) rates don't spike higher, well... stocks can probably continue to advance in the 8% - 12% per year range. Unless, of course, something comes out of the wood work to change the fundamental backdrop of course. But that never happens, right?

Thought For The Day:

Wanting to be someone you're not is a waste of the person you are. -Kurt Cobain

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of Tax Reform

2. The State of the Economic/Earnings Growth (Fast enough to justify valuations?)

3. The State of Geopolitics

4. The State of Fed Policy

Wishing you green screens and all the best for a great day,

David D. Moenning

Chief Investment Officer

Sowell Management Services

Disclosure: At the time of publication, Mr. Moenning and/or Sowell Management Services held long positions in the following securities mentioned: none. Note that positions may change at any time.

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.