How Low Can It Go?

Are we having fun yet? To be sure, the recent stock market correction has created some angst as the bears have knocked -7.55% off the DJIA, -9.63% off the S&P 500, -12.60% off the NASDAQ Composite, -12.86% from the Mid-cap index, and -15.69% from the Russell 2000 small-cap index. So, as they like to say on TV, most of the major indices are definitely in "correction territory."

However, the fact that the market corrected should not have come as a surprise to readers of this oftentimes meandering morning market missive. For example, back in July and August I began emphasizing the point that many of my favorite long-term market models were not in their happy places and that "risk was elevated."

And I am pleased to report that we did take some precautionary measures in various portfolio strategies to take both the beta and the exposure of the portfolios down a notch or two.

However, it is important to remember whilst patting one's self on the back that taking defensive measures is only half the battle! The next trick is to identify when the coast is clear and to attempt to benefit from the pullback.

Which brings us to the title of this week's macro market missive: How Low Can It Go?

Obviously, this is a tricky subject. And to review, I don't run portfolios based on my view or make market calls. No, on that note, I prefer to stick to the weight of the evidence from my major market models. However, experience has taught me that it can be tough to pull the trigger when the indicators tell you to take action - especially during emotional markets. Thus, having some sort of clue as to how far the bears could take things during times like these can help one prepare.

So this morning, I thought it would be good to review the history of cyclical bear market declines in various environments.

The History of Bear Attacks

To be clear, I don't know that we are currently in a cyclical, or what I like to call a "mini," bear market. And I do not see any evidence that the current secular bull is ending. However, I will admit that there is a decent chance that there may be some additional downside to endure. And as such, I'd like to get a feel for how much more selling to prepare for.

So here goes. If let's look back at all the bear markets since 1900. Ned Davis Research tells me that there have been 36 bear markets to review. And so that we are all on the same page, a cyclical bear market is defined here as either a 30% drop in the DJIA after 50 calendar days or a 13% decline after 145 calendar days.

Looking at the bear markets as a whole, the average decline has been -30.6% and the median has been -26.0%.

However, both the economic and secular backdrop at the time bears occurred makes an BIG difference!

For example, during secular bear phases (secular trends tend to last many years and contain multiple cyclical bulls and bears), of which there have 22 cases, the average decline has been -36.3%.

But, during the 14 secular bull markets that have occurred since 1900, the average decline of a "cyclical bear" is -21.8% and the median is -19.0%.

Currently, I believe the stock market is in the midst of a secular bull phase, which began on March 9, 2009. So, we can take solace in the fact that bear markets that occur during a secular bull are much shorter and shallower than average.

In addition, we can look at the damage the bears are able to inflict given the economic environment. I.E. Whether or not the U.S. economy is in recession. NDR's computers tell us that since 1960, the bear markets that occurred in association with a recession in the U.S., have produced an average decline of -30.5%.

But when the bears attacked without the U.S. being in recession, the 10 declines averaged -22.9%.

More recently, the last two cyclical bears occurred without an accompanying recession. In 2011, the fear over Greece and the U.S. debt downgrade produced a decline of -16.8% on the DJIA. And in 2015/16, the fear over China created a decline of -14.5%.

So, given that the Dow is currently down -7.6% and the S&P is off -9.6%, recent history suggest that the decline is at least half over. Assuming the current dance to the downside turns into a cyclical bear, that is.

The key here is that if you have cash put aside and the bears do take hold here, one strategy would be to start deploying capital into any further downside action.

Moving On... Now let's turn to the weekly review of my favorite indicators and market models...

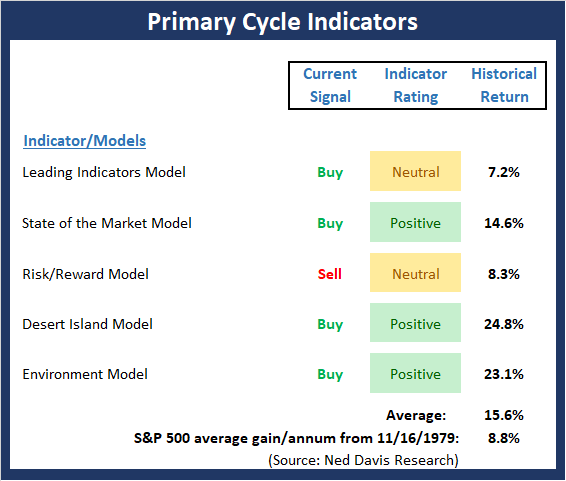

The State of the Big-Picture Market Models

I like to start each week with a review of the state of my favorite big-picture market models, which are designed to help me determine which team is in control of the primary cycle.

View My Favorite Market Models Online

The Bottom Line:

- The Primary Cycle board did a good job of alerting us to the fact that the odds of a correction were elevated - well before the current nastiness began. However, the model seems to be sending a different message now. So, unless the models weaken in the next month, my takeaway is that the current decline will wind up in the "correction" category as opposed to the "bear" camp. But time will tell here and we shall see.

This week's mean percentage score of my 5 favorite models pulled back a bit to 62.0 (from 64.0%) while the median held at 70% (also from 70%).

The State of the Trend

Once I've reviewed the big picture, I then turn to the "state of the trend." These indicators are designed to give us a feel for the overall health of the current short- and intermediate-term trend models.

View Trend Indicator Board Online

The Bottom Line:

- To no one's surprise, the Trend board remains negative to start the week. However, the good news is the cycle composite points higher this week and reminds us that favorable seasonality is just around the corner. It is also important to remember that the long-term trend model remains positive.

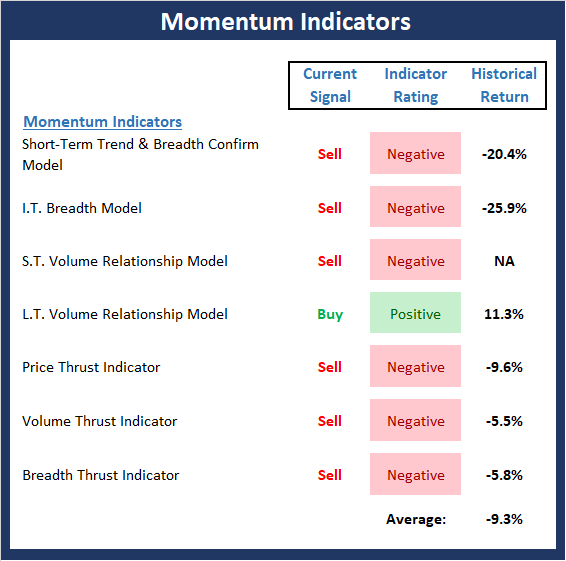

The State of Internal Momentum

Next up are the momentum indicators, which are designed to tell us whether there is any "oomph" behind the current trend.

View Momentum Indicator Board Online

The Bottom Line:

- The Momentum board remains an ugly sight to behold. The key here is there has been enough technical damage done that the bottom will likely be a process as opposed to an event. But then again, if we get good news on trade or Powell says the words "data dependent," things could change in a hurry.

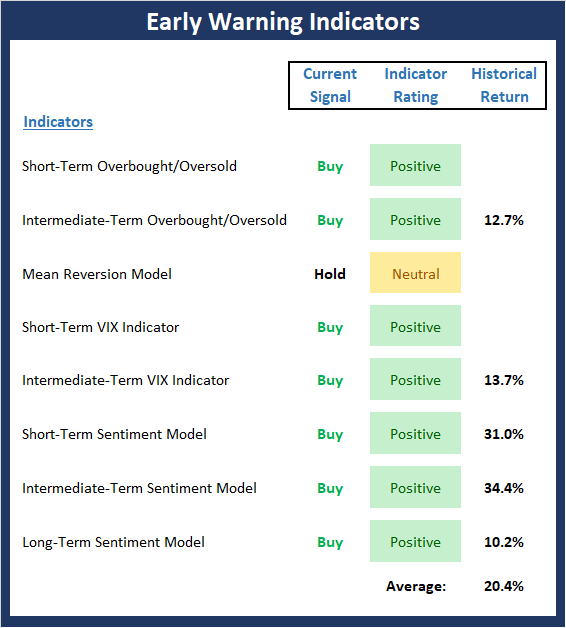

The State of the "Trade"

We also focus each week on the "early warning" board, which is designed to indicate when traders might start to "go the other way" -- for a trade.

View Early Warning Indicator Board Online

The Bottom Line:

- The "Early Warning" board, which, again did a great job of alerting us to the fact that the table had been set for the bears, now suggests that important oversold levels are being achieved. And the next "bounce" will likely be an important "tell" about what comes next from an intermediate-term trend perspective.

The State of the Macro Picture

Now let's move on to the market's "environmental factors" - the indicators designed to tell us the state of the big-picture market drivers including monetary conditions, the economy, inflation, and valuations.

View Environment Indicator Board Online

The Bottom Line:

- Analysts are fond of saying that the fundamental backdrop remains solid. By this, my guess is most are referring to the state of the economy and corporate earnings. However, when one looks beyond earnings, things become less encouraging. So, as I've been saying, this board reminds us that risk factors are elevated.

Thought For The Day:

Quality means doing it right when no one is looking. - Henry Ford

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

HCR Focuses on a Risk-Managed Approach to Investing

What Risk Management Can and Cannot Do

ANNOUNCEMENT:

HCR Awarded Top Honors in 2018 NAAIM Shark Tank Portfolio Strategy Competition

Each year, NAAIM (National Association of Active Investment Managers) hosts a competition to identify the best actively managed investment strategies. In April, HCR's Dave Moenning took home first place for his flagship risk management strategy.

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: none - Note that positions may change at any time.

Indicators Explained

Short-Term Trend-and-Breadth Signal Explained: History shows the most reliable market moves tend to occur when the breadth indices are in gear with the major market averages. When the breadth measures diverge, investors should take note that a trend reversal may be at hand. This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 5-day smoothing and the All-Cap Equal Weighted Equity Series is above its 25-day smoothing, the equity index has gained at a rate of +32.5% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +13.3% per year. And when both are below, the equity index has lost +23.6% per year.

Channel Breakout System Explained: The short-term and intermediate-term Channel Breakout Systems are modified versions of the Donchian Channel indicator. According to Wikipedia, "The Donchian channel is an indicator used in market trading developed by Richard Donchian. It is formed by taking the highest high and the lowest low of the last n periods. The area between the high and the low is the channel for the period chosen."

Intermediate-Term Trend-and-Breadth Signal Explained: This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 45-day smoothing and the All-Cap Equal Weighted Equity Series is above its 45-day smoothing, the equity index has gained at a rate of +17.6% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +6.5% per year. And when both are below, the equity index has lost -1.3% per year.

Cycle Composite Projections: The cycle composite combines the 1-year Seasonal, 4-year Presidential, and 10-year Decennial cycles. The indicator reading shown uses the cycle projection for the upcoming week.

Trading Mode Indicator: This indicator attempts to identify whether the current trading environment is "trending" or "mean reverting." The indicator takes the composite reading of the Efficiency Ratio, the Average Correlation Coefficient, and Trend Strength models.

Volume Relationship Models: These models review the relationship between "supply" and "demand" volume over the short- and intermediate-term time frames.

Price Thrust Model Explained: This indicator measures the 3-day rate of change of the Value Line Composite relative to the standard deviation of the 30-day average. When the Value Line's 3-day rate of change have moved above 0.5 standard deviation of the 30-day average ROC, a "thrust" occurs and since 2000, the Value Line Composite has gained ground at a rate of +20.6% per year. When the indicator is below 0.5 standard deviation of the 30-day, the Value Line has lost ground at a rate of -10.0% per year. And when neutral, the Value Line has gained at a rate of +5.9% per year.

Volume Thrust Model Explained: This indicator uses NASDAQ volume data to indicate bullish and bearish conditions for the NASDAQ Composite Index. The indicator plots the ratio of the 10-day total of NASDAQ daily advancing volume (i.e., the total volume traded in stocks which rose in price each day) to the 10-day total of daily declining volume (volume traded in stocks which fell each day). This ratio indicates when advancing stocks are attracting the majority of the volume (readings above 1.0) and when declining stocks are seeing the heaviest trading (readings below 1.0). This indicator thus supports the case that a rising market supported by heavier volume in the advancing issues tends to be the most bullish condition, while a declining market with downside volume dominating confirms bearish conditions. When in a positive mode, the NASDAQ Composite has gained at a rate of +38.3% per year, When neutral, the NASDAQ has gained at a rate of +13.3% per year. And when negative, the NASDAQ has lost at a rate of -10.27% per year.

Breadth Thrust Model Explained: This indicator uses the number of NASDAQ-listed stocks advancing and declining to indicate bullish or bearish breadth conditions for the NASDAQ Composite. The indicator plots the ratio of the 10-day total of the number of stocks rising on the NASDAQ each day to the 10-day total of the number of stocks declining each day. Using 10-day totals smooths the random daily fluctuations and gives indications on an intermediate-term basis. As expected, the NASDAQ Composite performs much better when the 10-day A/D ratio is high (strong breadth) and worse when the indicator is in its lower mode (weak breadth). The most bullish conditions for the NASDAQ when the 10-day A/D indicator is not only high, but has recently posted an extreme high reading and thus indicated a thrust of upside momentum. Bearish conditions are confirmed when the indicator is low and has recently signaled a downside breadth thrust. In positive mode, the NASDAQ has gained at a rate of +22.1% per year since 1981. In a neutral mode, the NASDAQ has gained at a rate of +14.5% per year. And when in a negative mode, the NASDAQ has lost at a rate of -6.4% per year.

Short-Term Overbought/sold Indicator: This indicator is the current reading of the 14,1,3 stochastic oscillator. When the oscillator is above 80 and the %K is above the %D, the indicator gives an overbought reading. Conversely, when the oscillator is below 20 and %K is below its %D, the indicator is oversold.

Intermediate-Term Overbought/sold Indicator: This indicator is a 40-day RSI reading. When above 57.5, the indicator is considered overbought and when below 45 it is oversold.

Mean Reversion Model: This is a diffusion model consisting of five indicators that can produce buy and sell signals based on overbought/sold conditions.

VIX Indicator: This indicator looks at the current reading of the VIX relative to standard deviation bands. When the indicator reaches an extreme reading in either direction, it is an indication that a market trend could reverse in the near-term.

Short-Term Sentiment Indicator: This is a model-of-models composed of 18 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a short-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Intermediate-Term Sentiment Indicator: This is a model-of-models composed of 7 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from an intermediate-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Long-Term Sentiment Indicator: This is a model-of-models composed of 6 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a long-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Absolute Monetary Model Explained: The popular cliché, "Don't fight the Fed" is really a testament to the profound impact that interest rates and Fed policy have on the market. It is a proven fact that monetary conditions are one of the most powerful influences on the direction of stock prices. The Absolute Monetary Model looks at the current level of interest rates relative to historical levels and Fed policy.

Relative Monetary Model Explained: The "relative" monetary model looks at monetary indicators relative to recent levels as well as rates of change and Fed Policy.

Economic Model Explained: During the middle of bull and bear markets, understanding the overall health of the economy and how it impacts the stock market is one of the few truly logical aspects of the stock market. When our Economic model sports a "positive" reading, history (beginning in 1965) shows that stocks enjoy returns in excess of 21% per year. Yet, when the model's reading falls into the "negative" zone, the S&P has lost nearly -25% per year. However, it is vital to understand that there are times when good economic news is actually bad for stocks and vice versa. Thus, the Economic model can help investors stay in tune with where we are in the overall economic cycle.

Inflation Model Explained: They say that "the tape tells all." However, one of the best "big picture" indicators of what the market is expected to do next is inflation. Simply put, since 1962, when the model indicates that inflationary pressures are strong, stocks have lost ground. Yet, when inflationary pressures are low, the S&P 500 has gained ground at a rate in excess of 13%. The bottom line is inflation is one of the primary drivers of stock market returns.

Valuation Model Explained: If you want to get analysts really riled up, you need only to begin a discussion of market valuation. While the question of whether stocks are overvalued or undervalued appears to be a simple one, the subject is extremely complex. To simplify the subject dramatically, investors must first determine if they should focus on relative valuation (which include the current level of interest rates) or absolute valuation measures (the more traditional readings of Price/Earnings, Price/Dividend, and Price/Book Value). We believe that it is important to recognize that environments change. And as such, the market's focus and corresponding view of valuations are likely to change as well. Thus, we depend on our Valuation Models to help us keep our eye on the ball.

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.