Looking Ahead: The Correction Will End When...

It is said that stock market corrections are only "normal and healthy" until you are in the middle of one. The problem is it can be tough to see the bright side of the macro picture when volatility begins spiking, prices start to crater (and then recover, and then crater again), and all kinds of scary arguments/narratives start to be made in the popular financial media.

From my seat, this is exactly what the stock market is going through right now - a corrective phase. Or call it a consolidation. Or, as I like to say, a sloppy period. A period in which the way forward starts to look a bit cloudy or perhaps even downright stormy.

Again, while this is just my opinion, traders appear to be looking for clarity on a number of issues right now. And until we get a better view, the road ahead might be a little bumpier than normal.

Probably the most important "issue" traders are dealing with here is the reality that growth is slowing. To be clear, this does not mean a recession is imminent. No, the issue here is we're seeing the RATE of growth slow.

As we've discussed a time or two, this was to be expected at some point. Remember, the explosive economic and earnings growth rates seen in recent quarters were artificially high - because the economy had been intentionally shut down, and then reopened on a dime. So, BAM, you got some eye-popping growth when things reopened and were juiced by all the stimulus from Washington.

So, with the stimulus now wearing off and the initial surge behind us, the question becomes, what does future economic growth look like? Will it be 4% as many Wall Street firms are projecting? And if so, for how long? Or will we return to the more pedestrian growth rates seen pre-COVID (I.E. Something in the 2-2.5% zone)?

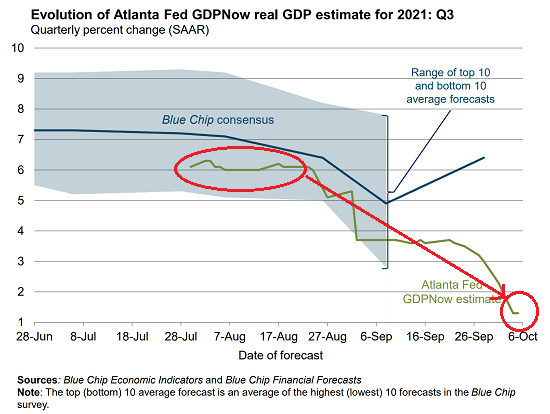

Here's an example of my point. In mid-August, the Atlanta Fed's GDPNow (a real time estimate of GDP growth) for the 3rd Quarter was sitting comfortably above 6%. This meant that, at the time, GDP was growing at a 6% annual clip. Now fast-forward to early October, you know, after Delta put a big 'ol crimp in everyone's return-to-normal plans. As of October 6, the Nowcast had fallen to just 1.3%. Ouch.

Image Source: Atlanta Fed

From my seat, this is really the crux of the reason why stocks stopped dancing merrily higher when the calendar page flipped to September. In short, economic reality set in. And right now, the future doesn't look near as bright as it did back in the summer. As such, a 4-5% pullback seems to make some sense - well, to me, anyway.

Additional pieces of evidence here include Goldman Sachs dropping their 2022 GDP estimate this week from 4.4% to a still upbeat 4.0%. Goldman's team cited expiring stimulus, a slowdown in consumer spending, supply chain issues worsening, and the general economic drag created by the Delta surge as the reasons for the cut. Seems logical.

But #GrowthSlowing isn't the only thing weighing on traders' collective psyches. In addition, there is the worry about stagflation (defined as stagnating economic growth and increasing inflation), the earnings season, Fed policy, the status of Chair Powell, and, of course, China. Ugh.

Even Apple (AAPL) got into the mix Tuesday afternoon by announcing they were cutting iPhone production by 10 million units due to, everybody now... chip shortages. So, heck, if the biggest company on the planet can't figure this out, I guess we really do have some issues to noodle on.

I could go on (and on) about any/all of the above. But the bottom line - at least in my brain - is that traders just don't know what the future looks like. And there are lots and lots of questions. How long will it take for the chip shortage to get fixed? When will supply chain issues stop impacting prices? When will there be enough truckers to get everything to where it needs to go? When will prices of "stuff" stop rising? Are rising wages here to stay? And so on, and so on.

So, until we can get some clarity of some of these issues, we should probably expect to see more of this sloppy period. As such, we probably shouldn't be surprised to see some additional volatility in both directions - or for the computers to freak out every now and again. It's just the way the game is played these days.

For me, I take comfort in the smallish amount of dry powder I have in portfolios. Because at some point, the corrective phase will end and a dip-buying opportunity may arise. Fingers crossed.

Thought for the Day:

Life can only be understood backwards, but must be lived forwards. -Soren Kirkegaard

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research, a Registered Investment Advisor

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: AAPL - Note that positions may change at any time.

NOT INDIVIDUAL INVESTMENT ADVICE. IMPORTANT FURTHER DISCLOSURES