Not So Fast, Please

To be sure, what I like to call "Fed Expectations" has been the primary driver of the market action for some time now. You know the drill. When economic data or Fedspeak supports the idea of rate cuts in the near future, stocks rise. And vice versa. Simple, right? From my seat, this and the state of corporate earnings is all anyone really needs to focus on these days.

Traders also seem to be particularly sensitive to when the Fed will cut rates as well as how many times Jay Powell & Co plan to reduce rates in calendar year 2024. The thinking is that if rates can come down sooner rather than later, the risk of the economy faltering is lower.

This certainly makes sense as one of the primary fears in the market over the current hiking cycle has been that the Fed will, as usual, go too far. (The U.S. Central Bank does have a long history of overdoing it!) In short, the worry is they will raise rates too much and/or hold rates too high for too long... and wind up causing economic damage in the process.

However, history - as well as the computers at Ned Davis Research - suggests that the Fed Chairman and his merry band of central bankers should take their time and cut rates slowly.

Frankly, this concept, while historically sound, might seem a bit counterintuitive. After all, doesn't corporate America need the central bank to remove its foot from their collective throats as quickly as possible? Won't earnings be at risk if the Fed doesn't act soon?

In short, the answer is no. The real key here isn't necessarily when the Fed takes action, but rather how the economy fares while the Fed is cutting rates.

You see, if the Fed is cutting rates quickly, it likely means there is either some sort of crisis afoot (a war, bank collapse, terrorist attack, etc) or that the economy needs rescuing because its already in recession. But since the stock market is a discounting mechanism of future expectations, stocks tend to rise once the Fed reducing rates - even when the economy is in recession, albeit relatively slowly.

Yet when the Fed employs a slow approach to reducing rates, it means the economy likely isn't in dire straits. Thus, when the Fed starts an easing cycle, the market tends to respond more robustly. From my perch, this is due to the idea that earnings are expected to improve quickly with the economic backdrop remaining sound.

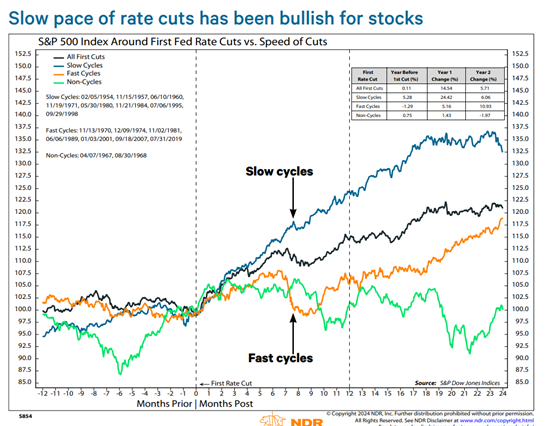

Below is a chart from Ned Davis Research illustrating the history of "fast" versus "slow" rate cutting cycles. The top line in blue represents the action of the S&P 500 when the Fed has cut rates slowly, while the orange line shows what happens to stocks when the Fed is forced to cut rates quickly.

View Larger Chart

Copyright Ned Davis Research Group, All Rights Reserved

The numbers don't lie. When the Fed takes it slow, stocks have gained more than 24% on average one year after the first rate cut. But when the Fed has to act quickly, the gains are just a hair over 5%, which is well below the historical average for all annual returns.

Two years after the Fed starts cutting rates, the spread remains strong. Slow cycles have produced average cumulative gains of more than 32% while gains after fast rate-cut cycles begin are less than 20%.

What's Happening Now

The question, of course, is what we should expect now. My take is that traders expect the Fed to "go slow" this time around due to the fact that the economy is doing just fine, thank you. Thus, traders may be jumping the gun and "pulling forward" the gains that tend to occur after the Fed starts cutting rates.

And yes, the enthusiasm and explosive growth seen in the AI space is certainly lending a hand here. But the bottom line is odds seem to favor the bulls here and therefore, a "buy the dips" approach makes a lot of sense to me - for now, anyway.

Thought for the Day:

You cannot escape the responsibility of tomorrow by evading it today. -Abraham Lincoln

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research, a Registered Investment Advisor

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: None - Note that positions may change at any time.

NOT INDIVIDUAL INVESTMENT ADVICE. IMPORTANT FURTHER DISCLOSURES