The Trend Is Your Friend, But...

Good Monday - oops, I mean Tuesday morning and welcome back. Although the drama in D.C. continues to build on several topics and I continue to be asked what my "Trump Contingency Plan" is in case of trouble (short answer: I don't have one - nor do I have "Trump Success Plan" - we manage money based on what the market "is" doing and not what we thing it ought to be doing!), market players continue to discount greener economic pastures via fresh all-time highs in the major market indices. But before we get too carried away with any further prognostications, let's review my key market models and indicators.

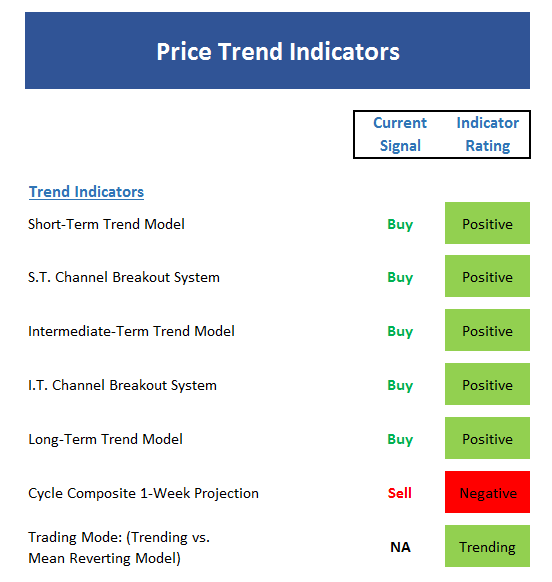

The State of the Trend

We start each week with a look at the "state of the trend" from our objective indicator panel. These indicators are designed to give us a feel for the overall health of the current short- and intermediate-term trend models.

Executive Summary:

- The most bullish thing a market can do is make new highs. We could probably end this week's report right there

- The short-term Channel Breakout system is now in trending mode. This means a less sensitive approach is in order.

- Short take on state of intermediate-term trend: All good

- Intermediate-term Channel Breakout system favors Bulls as long as S&P remains above 2250

- No complaints from long-term trend perspective

- Cycle Composite is negative again this week but then turns up for the next two

- Trading vs. Trending? Duh...

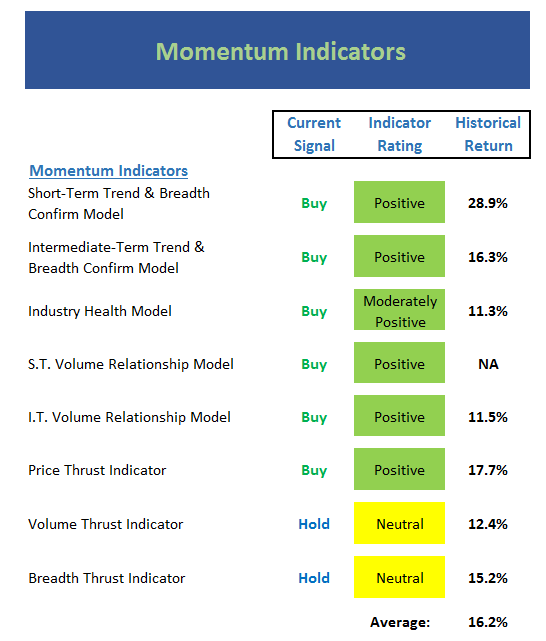

The State of Internal Momentum

Now we turn to the momentum indicators...

Executive Summary:

- Both the short- and intermediate-term Trend & Breadth Confirm models are in gear

- The Industry Health model still not outright positive. This is likely due to falling sector correlations and the rapid rotation seen over past 6 months.

- The short-term Volume Relationship model is positive, but not great

- The intermediate-term Volume Relationship model is strong

- Not surprisingly, the Price and Breadth Thrust indicators are positive

- But, Volume Thrust tells me there is a lack of conviction (so far)

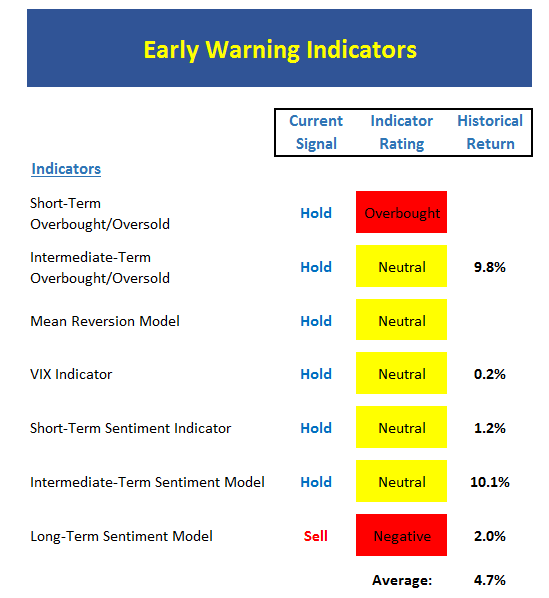

The State of the "Trade"

Next up is the "early warning" board, which is designed to indicate when traders may start to "go the other way" -- for a trade.

Executive Summary:

- With the largest pullback since early November being just -0.43%, we conclude that this is a "good overbought" condition

- Market overbought on all 3 time frames - at some point, this will matter

- Our Mean Reversion model close to issuing a buy signal - tells me a strong trend is underway

- The VIX Model is currently in Neverland... can't move far enough in either direction to issue a signal

- Short-term VIX just issued a trading buy (but this could be a very short signal)

- All 3 Sentiment models are now squarely negative

- Highest degree of optimism on our long-term Sentiment model since late 2014

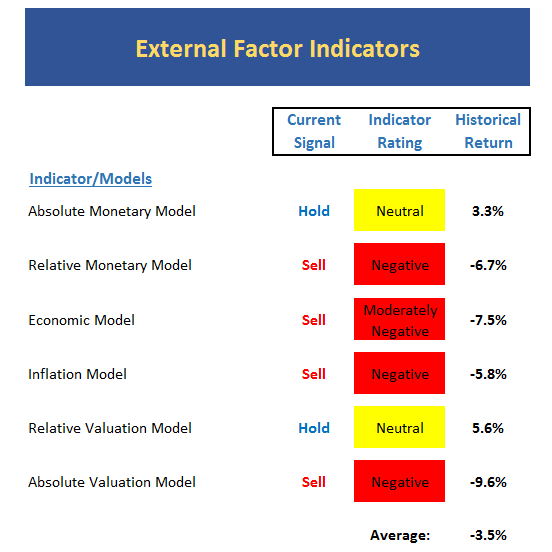

The State of the Macro Picture

Now let's move on to the market's "external factors" - the indicators designed to tell us the state of the big-picture market drivers including monetary conditions, the economy, inflation, and valuations.

Executive Summary:

- This board continues to be a mess and should be viewed as a warning flag

- Monetary models continue to decline

- The Econ model is rebounding from its low. Obviously this model is currently out of sync with market, but the historical returns of the model are double the SPX since 1965

- Inflationary pressure continues to build. Another inflation model (not shown) closing in on "strong inflationary" zone

- Relative Valuation model continuing to move down in neutral zone. Recall that this model had been positive for several years.

- The historical return average is negative. This is largely due to monetary models but remains something to watch.

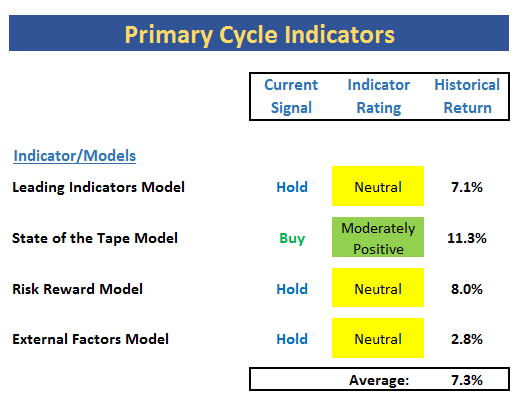

The State of the Big-Picture Market Models

Finally, let's review our favorite big-picture market models, which are designed to tell us which team is in control of the prevailing major trend.

Executive Summary:

- The Leading Indicators model - which did the best job of signaling both start and end of recent mini bear - moved back up into moderately positive zone from neutral.

- Tape Model still green

- The Risk/Reward model continues to be hurt by monetary and sentiment model readings

- The model build on external factors is moving the wrong direction and currently sports the weakest reading since 2010

- Average return of the board is in line with historical mean

The Takeaway...

As the saying goes, the trend is your friend. However, we do NOT believe this is a low risk environment given that monetary and inflation models are heading in the wrong direction, stocks are overbought, and sentiment has reached extreme levels. But to be clear, none of the above is a reason to sell. From my seat, this is an environment where prudence should take the place of greed - meaning that this is not the time to have one's foot to the floor. And finally, the readings of our bigger picture models suggest that we need to stay alert for something that could disrupt the trend of discounting a stronger than anticipated economic and earnings picture.

Thought For The Day:

"I believe fundamental honesty is the keystone of business." - Harvey Firestone

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of Trump Administration Policies

2. The State of the U.S. Economy

3. The State of Global Central Bank Policies

Wishing you green screens and all the best for a great day,

David D. Moenning

Chief Investment Officer

Sowell Management Services

Looking for a "Modern" approach to Asset Allocation and Portfolio Design?

Looking for More on the State of the Markets?

Investment Pros: Looking to modernize your asset allocations, add risk management to client portfolios, or outsource portfolio Management? Contact Eric@SowellManagement.com

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.