Tidbits to Ponder

One of the most important lessons to learn in the business of investing is to think for yourself. As a young portfolio manager, the tendency is to try and read everything you can and to listen to everyone. While the desire to learn is a good thing, the problem with a shotgun approach to information is there are simply too many opinions out there - many of which are misguided, uninformed, or just plain wrong. Thus, the bottom line is listening to too many people can lead to decision gridlock.

At the same time, you definitely need input from time to time in this business because it is virtually impossible to master the investing game. In my opinion, the trick is to (a) limit the inputs you receive and (b) to have a thorough understanding of the approach/philosophy employed by the folks you are listening to.

For example, I am often asked if I read so-and-so's latest view on the market's next move. My answer is almost always the same, "No, so-and-so is not a member of my inner circle." And in my mind, I quietly add, "Thus, I don't give a hoot what they said/think."

To be sure, this can come off as cocky at times. But I'm not saying that so-and-so isn't smart, doesn't have value, or that their opinion is wrong. No, I'm simply saying that I limit the number of people I allow to influence my thought process and so-and-so isn't on the list. The key here is you need to know what you stand for in terms of investing philosophy.

With that said however, listening to the message of "the crowd" can be very helpful at times. You see, at least part of the investing game is about "money flows." The action in the FAANGs (Facebook, Apple, Amazon, Netflix, Google) over the past year is a perfect example. In short, these stocks have become must-own positions for portfolio managers. And yes, when the market eventually does decline, this is not going to be a good place to be. But in the meantime, understanding where the big boys are putting their money can help you understand what is happening.

For this reason, I like to pay attention to a few surveys throughout the year. First, I always spend time with the list from Goldman displaying the 50 biggest positions hedge funds hold. In short, this tells me what the big money is actually "doing" (as opposed to what the managers are "saying" - remember "talking your book" is still legal). For the record, the current list of stocks that most frequently appear among the largest 10 holdings of hedge funds include: Facebook (FB), Amazon.com (AMZN), Alibaba Group (BABA), Time Warner (TWX), Alphabet (GOOGL), Charter Communications (CHTR), Microsoft (MSFT), NXP Semiconductors (NXPI), Visa (V), and, of course, Apple (AAPL).

This morning, another "outside input" hit my inbox - the Merrill Lynch Fund Manager Survey. Again, reviewing this type of data helps me understand what the big money is thinking/doing so that I don't bonk on any big trend in the markets. In reviewing the data, I found a few points interesting, so I thought I'd pass them along.

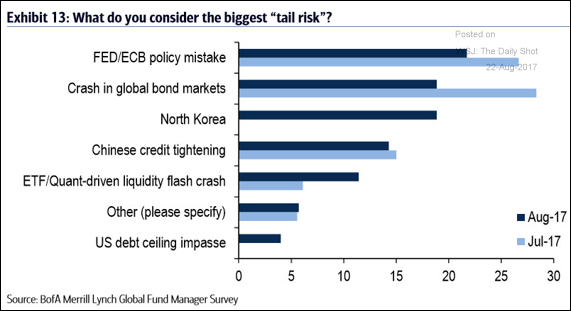

Managers are Watching Korea

While it is easy to dismiss the geopolitical games being played by the kid running North Korea, apparently fund managers are taking this seriously.

As the chart below shows, North Korea showed up in this month's list of "tail risks." Note that the potential for an impasse on raising the debt ceiling next month also made the list for the first time...

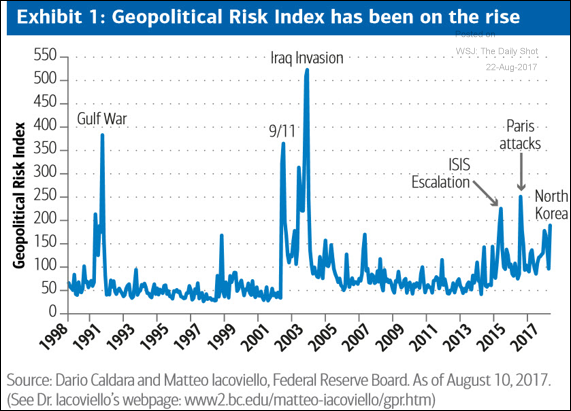

The Term "Geopolitical Risk" is Back

Although the market isn't easily influenced by external and/or terrorist events these days, the index tracking geopolitical risk is definitely rising.

Valuations Are a Concern

Next up on managers' hit parade of worries is the issue of stock market valuations. Note that this is not a chart of stock market valuation levels, rather a chart of the percentage of managers who think the equity markets are overvalued.

As the WSJ points out today, this group didn't see a problem with valuations in 2006-07. As such, one can argue that this next chart could be considered a contrarian view.

Countering this thought however, was the view that stocks were clearly overvalued back in 1999. So, at this time, I'm going to opine that valuations are indeed an issue to be concerned about - if and when a negative catalyst arises, that is.

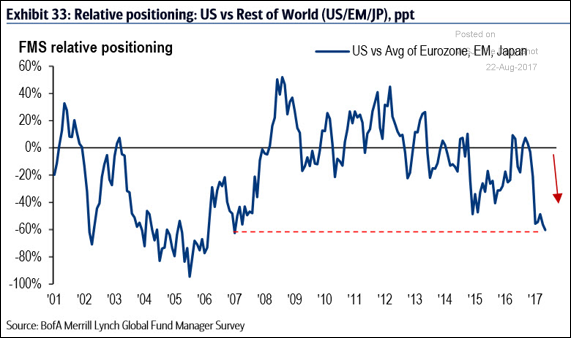

The Great Rotation: Managers Looking Overseas for Values

The next chart confirms the view that fund managers as a whole are moving money overseas. The thinking here is that places like the Eurozone, the Emerging Markets, and Japan provide better values for those managers who are required to be fully invested at all times. So, these managers appear to be rotating out of the U.S. and into foreign markets.

Profits Could Be a Problem

It is said that earnings are the Mother's Milk of the stock market. But in reality, it is earnings expectations that tend to set the stage during the quarterly earnings parade. And the key takeaway from the next chart is the fact that the percentage of managers expecting corporate profits to improve is declining.

One way to look at this is that expectations are falling, which would allow companies the opportunity to "surprise to the upside." However, if managers begin to see profits trending lower, valuations could become an issue.

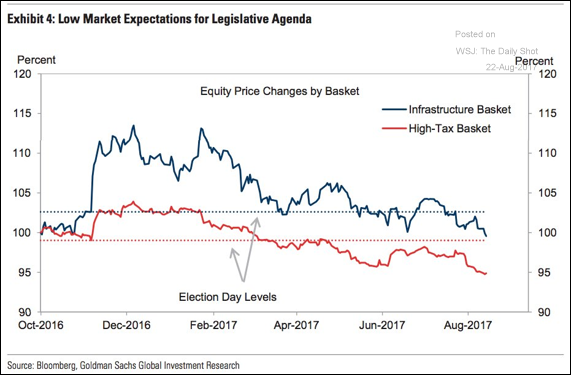

Trump Trade Comes Off

And finally, there appears to be proof that the so-called "Trump Trades" are no longer a primary driver of this market.

The chart below shows the price action of two "baskets" of stocks. The blue line represents a basket of stocks that would benefit from infrastructure spending. The red line is a basket of stocks perceived to benefit from tax reform. And the gray dotted lines represent the levels of each on election day.

As you can plainly see, both baskets are (a) below the levels seen at the time of the election, (b) below the peak levels of 2017, and (c) trending down. Thus, it is easy to argue that "legislative agenda" is no longer "baked in" to the market's cake.

It is my sincere hope that you find these tidbits of information helpful; I certainly did.

Thought For The Day:

If we all make mistakes, what separates the winners from the losers? The answer is simple – the winners make small mistakes while the losers make big mistakes. -Ned Davis

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of the Trump Administration

2. The State of the Economic/Earnings Growth (Fast enough to justify valuations?)

3. The State of Geopolitics

4. The State of Fed Policy

Wishing you green screens and all the best for a great day,

David D. Moenning

Chief Investment Officer

Sowell Management Services

Disclosure: At the time of publication, Mr. Moenning and/or Sowell Management Services held long positions in the following securities mentioned: none. Note that positions may change at any time.

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.