Two Charts Explain The Action

Here we go again. Apparently the fast money traders and their computers have decided that another fast-moving, violent rotation in the stock market is needed here. So, it's everybody out of the pool in tech in favor of players going all-in on the reopening/value stocks. Got it.

To be sure, we've seen this movie before. Late last fall, with the megacap tech names having pounded their value brethren into oblivion based on the view that "dependable growth" was the place to be, a similar rotation began. At the time, it made sense. The country was getting vaccinated, and everyone was looking ahead to better days - and a return to some sort of "normal life."

As such, the "rotation trade" was on. In turn, the Russell 2000 experienced the biggest/fastest rally in its history. All the while, traders were funding their buys in financials, airlines, cruise companies, energy, hotels, etc. with sales of those megacap growth names that we had all grown to know and love.

So, for a spell, it looked like the unloved value space, which hadn't outperformed growth in what felt like forever, was back - in a big way. But as tends to be the case on Wall Street, the "trade" into value/reopening plays quickly became overdone.

Before too long, those value plays, which aren't curing cancer or changing the way the world works/shops/eats, etc., started to look a little pricey - especially compared to the big tech names that print money every quarter. As I reminded clients at the time, it was important to recognize that John Deere can only sell so many tractors. Thus, the increases in the P/E's could really only go so far.

What happened next? Yep, that's right, the rotation trade reversed - thanks to the surge in the Delta variant. Cases in places like the U.K. and India were going up in a scary way. And reports of "breakthrough infections" caused folks to question their behavior Suddenly, the "new normal" looked like it might be delayed, postponed, or worse.

On Wall Street, value was out, and dependable growth was back in. Makes sense, right?

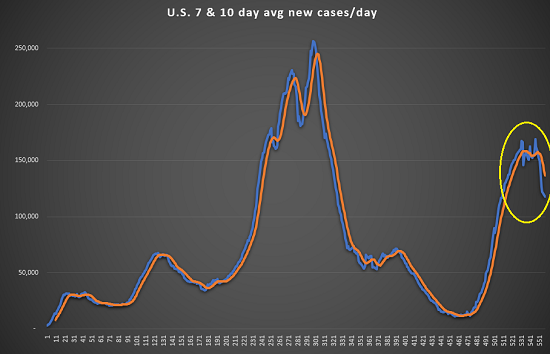

Now fast-forward to the beginning of this week. Word was the Delta surge was starting to roll over, which, of course makes the "reopening" stock space look attractive again. And the numbers supported the thesis (see chart below).

{kind=link}

In addition, traders in the bond market started to rethink the "lower for longer" theme and seemingly embraced the idea that the "taper" was coming. This time for sure.

Recall that just last week, Fed Chairman Powell had told us to expect the central bank to start reducing the amount of bonds they would be buying each month. And while Powell reassured everyone that the "taper" did NOT equate to the beginning of a rate-hiking cycle, the bottom line is starting in November, there would likely be fewer buyers in the bond market each month.

Now toss in the "sausage making" process playing out in D.C. over the debt ceiling (which, of course, includes talk of the U.S. defaulting on its debts), and well, an increase in interest rates makes sense.

Below is a chart of the yield on the U.S. 10-year Treasury, which looks to be telling a story here.

U.S. 10-Year Yield

View Larger Chart

{kind=link}

So, there you have it. With the reopening stocks playing catchup due to a decline in COVID cases and the bond market doing a rethink based on the Fed's new stance, it looks like traders have told their computers to hit play on the buy-reopening/value, sell-tech game.

The question, of course, is how long will this particular "trade" last? Is this an end-of-quarter thing, or a theme that may take hold for the foreseeable future? Time will tell, of course.

Oh, and how does the inflation situation get factored in going forward? Don't look now fans, but energy is surging due to shortages, supply chain problems, etc. Barron's referenced a "developing global energy crisis" in a report this morning. And with winter coming, well, it is easy to see how this trade could also take root. Which, in turn, would/could boost those inflation numbers.

P.S. I think today's quote of the day is especially appropriate for the way the markets behave these days!

Thought for the Day:

One dog barks at something. And a hundred dogs bark at the sound. - Chinese Proverb

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research, a Registered Investment Advisor

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: None - Note that positions may change at any time.

NOT INDIVIDUAL INVESTMENT ADVICE. IMPORTANT FURTHER DISCLOSURES