Two "Game Changers" Improve Outlook

Executive Summary:

The combination of Abbott's new rapid COVID test and Jay Powell's announcement that the Fed is taking a new tack on their approach to inflation pushed the S&P 500 to another all-time high on Thursday. While both can be viewed as "game changers," the realization that the Fed won't be embarking on any preemptive rate hikes if/when inflation rises means rates are likely to stay near zero for longer than even the most ardent bulls had expected. And this, dear readers, looks to be the real key to the fundamental backdrop to this market.

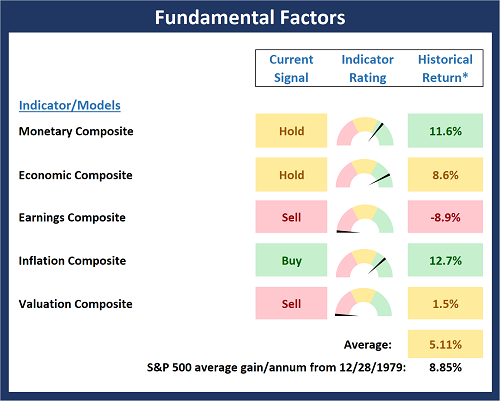

The State of the Fundamental Models...

There are no changes to report on the Fundamental Factors board this week. However, I will contend that the Fed's major policy shift announcement effectively should cause Monetary conditions toward a very bright shade of green. Since the idea of an "average inflation target" is brand new, it will be interesting to see if any of our monetary indicators will pick up on this over time. But for now, the Fundamental board is largely neutral.

View Fundamental Indicator Board Online

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

About Yesterday's Rate Move

In light of the fact I am arguing that Jay Powell and Company's new approach to inflation will be a positive for monetary conditions, you may be wondering why the yield on the 10-year spiked 6 bps yesterday. While 6 basis points (0.06%) doesn't sound like much, the move represented an 8.6% increase in yield. Thus, one might argue that the bond market reacted negatively to Powell's announcement.

US 10-Year Yield - Weekly

View Larger Chart

{kind=link}

However, I will contend that the move up in yields was more likely connected to the news that Abbott Labs has a cheap, accurate, and fast COVID test.

Exhibit A in my case here is the action in the airlines and other industries that can't function with social distancing requirements. Stocks like United Airlines (UAL) and Marriott (MAR) which are poster children for this space enjoyed good days, rising 5.75% and 4.5% respectively.

In addition, as the weekly chart of the 10-year shows, yields did move up yesterday. Yet the primary trend is still down.

For me, the bottom line is that if the public can get access to cheap, accurate, and fast COVIC tests, then some semblance of normalcy could possibly be on the horizon. Especially when you combine such testing with the upbeat news on the vaccine front. And if a return to "normal" is something investors can begin to entertain, then one has to be optimistic about both the economy and stock prices.

Thought For The Day:

He is richest who is content with the least -Socrates

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: none - Note that positions may change at any time.

Fundamental Models Explained

Monetary Composite: The popular cliche, "Don't fight the Fed" is really a testament to the profound impact that interest rates and Fed policy have on the market. It is a proven fact that monetary conditions are one of the most powerful influences on the direction of stock prices. The Monetary Composite is a combination of two proprietary monetary models developed by Ned Davis Research. The first is comprised of 14 indicators and is plotted as a composite and the second is made up of eight monetary-related indicators including money supply, and the bond and commodities markets.

Economic Composite: During the middle of bull and bear markets, understanding the overall health of the economy and how it impacts the stock market is one of the few truly logical aspects of the stock market. The economic composite is a series of three models designed to indicate the current state of the economy.

Earnings Composite: A series of four models designed to indicate the overall health of corporate earnings. The first model is based on the slope of the smoothed S&P 500 earnings per share. The second model looks at the drivers of earnings and includes indicators such as U.S. industrial production, the CRB Spot Raw Industrial Material Price Index, the Treasury yield curve, Institute for Supply Management (ISM) indices, corporate bond credit spreads, unemployment claims, and the trend in analyst earnings estimate revisions for the S&P 500. The third model is designed to indicate the likely trend in the earnings per share reported for the S&P 500 Index. This model uses a variety of macro variables to indicate whether current conditions are favorable for strong, moderate, or weak growth in S&P 500 earnings. The fourth model the median 12-month percent change in the one-year analyst forecast out of the 500 components of the index.

Inflation Model: From an historical perspective, one of the best "big picture" indicators of what the market is expected to do next is inflation. The Inflation model is designed to identify cyclical changes in the rate of inflation. The model consists of 22 individual indicators primarily measuring various rates of change of such indicators as commodity prices, the Consumer Price Index (CPI), producer prices, and industrial production.

Valuation Composite: If you want to get analysts really riled up, you need only to begin a discussion of market valuation. While the question of whether stocks are overvalued or undervalued appears to be a simple one, the subject is actually extremely complex. The Valuation composite consists of five valuation indicators/models developed by Ned Davis Research. The first valuation indicator reviews the S&P 500 Price-to-Earnings GAAP Ratio relative to normal, expensive, and bargain valuation zones. The second model measures the S&P 500’s Median P/E ratio, representing the median P/E of the 500 stocks in the index. The third model measures the Median P/E ratio of a multi-cap stock index. The fourth indicator is the P/E ratio of the Value Line Index. The fifth model is a composite of 7 indicators designed to reflect stock market valuations based on how various valuation indicators compare to their latest 10-year historical ranges.

NOT INVESTMENT ADVICE. The opinions and forecasts expressed herein are those of Mr. David Moenning and Heritage Capital Research and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning of Heritage Capital Research is an investment adviser representative of Eastsound Capital Advisors, LLC, a registered investment advisor. The adviser may not transact business in states where it is not appropriately registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

Mr. Moenning and Heritage Capital Research may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

The author neither endorses nor warrants the content of this site, any embedded advertisement, or any linked resource. The author or his managed funds may hold either long or short positions in the referenced securities. Republication rights must be expressly granted by author in writing.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.