A Look At The Big-Picture

The original purpose for my oftentimes meandering morning market missive was to identify the driving forces behind the market action. The thinking was that putting to paper (so to speak) my thoughts on why Ms. Market was doing what she was doing from a short-term perspective, I stood a better chance on staying in tune with the primary trend of the market. Or put another way, I was unlikely to wake up one day and wonder what the heck was going on.

Coupling (a) an understanding of what the market "is" doing and why (as opposed to offering up I think it "should" be doing, which, as I've learned, is a fool's errand) on both a short- and longer-term basis, (b) a rigorous review of a broad swath of market indicators/models, and (c) a set of rules to live by, basically defines my approach to money management. The bottom line is to avoid getting fooled and the "big mistake," which can crush portfolios and a money manager's career.

So, this morning I thought I'd go back to my roots and try to identify what is driving the current leg higher in the market.

We start with the question of what "is" happening in the current market. So, I'll begin by saying that this rally has surprised a lot of folks, including me. While I don't manage money based on my "view" of what ought to happen next in the game, I am not devoid of opinions on the subject. And the key is I figured trade concerns might keep the major indices bottled up for a while.

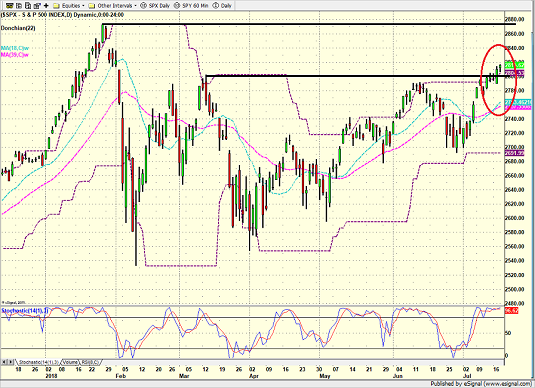

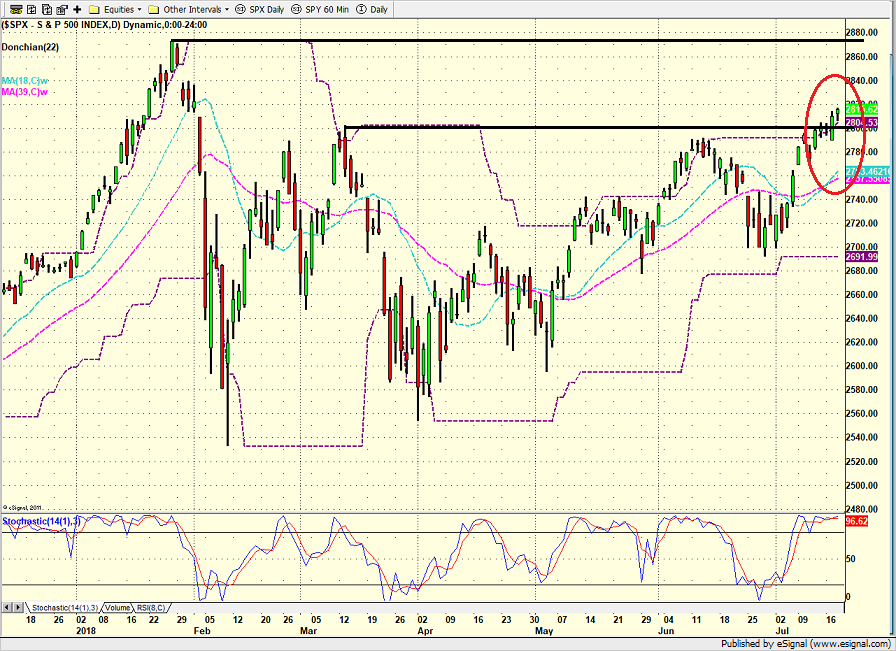

But, as the chart below illustrates, the S&P 500 has broken out of its recent 4.5-month trading range.

S&P 500 - Daily

View Larger Image Online

{kind=link}

While the jury is still out on whether the venerable blue-chip index can turn this break into new all-time highs during the current run, it does appear that the bulls are in control of the ball at the present time.

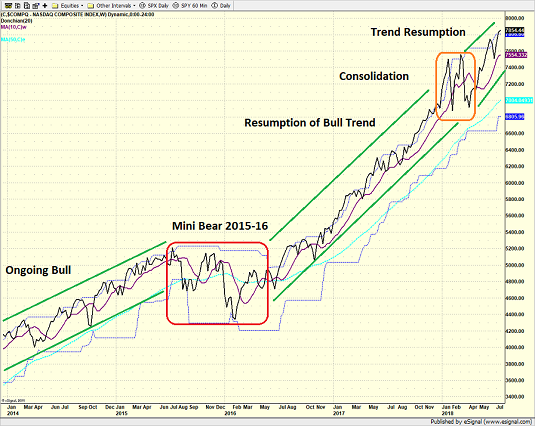

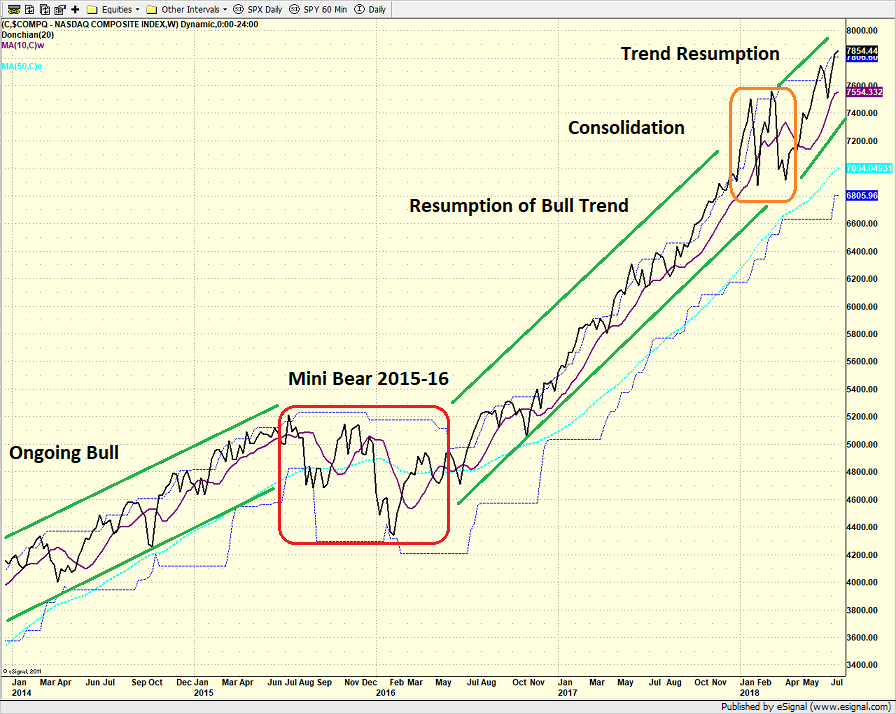

The big-picture becomes clearer when one looks at a longer-term (weekly) chart of the action over in four-letter land, (aka the NASDAQ Composite), which has been the leading index for many moons now.

NASDAQ - Weekly

View Larger Image Online

{kind=link}

This chart goes back to 2014. Recall that the bulls had been running hard since 2012 as the European Debt Crisis began to fade and traders focused on QE, and the idea that the U.S. wasn't going to slip into recession.

This run ended in the summer of 2015 as analysts began to worry about growth. More specifically, China's growth and the fact that the second largest economy in the world was slowing.

The three-year old bull then morphed into what I'll call a "Mini Bear," which ran from mid-2015 into February 2016. The bear ended abruptly when "Super Mario" (ECB President Mario Draghi) announced what was referred to at the time as "QE-Infinity." In short, Draghi let the world know that he and his central banker cohorts weren't about to let the markets slip back into crisis mode.

From there, the bulls ran, and ran hard, into January 2018. You remember January, don't you? Everything was wonderful and going to get even better for as far as the eye could see.

With investor sentiment at all-time highs and everyone on the planet able to recite the bull case, it is little wonder that stocks then consolidated the big gains for a spell.

It was during this consolidation phase, which appears to be over when looking at the NASDAQ and the Small-Caps, yet still intact on the S&P, that traders began to worry about "peak growth" in both the economy and earnings. As well as stuff like a trade war, political instability, geopolitical issues, the Fed, inflation, the yield curve, etc.

Which brings us to this morning, where we find ourselves looking at a modestly red open on more tough talk on trade. This, of course, brings the most recent "breakout" on the S&P into play and the possibility of yet another "fakeout."

Summing up, I believe the current dash for the border is being sponsored by a few things. First, the unexpectedly dovish Congressional testimony by Jerome Powell, who provided a level-headed view of the economy and the Fed's approach to monetary policy. Second, the expectation that the current "trade war" will wind up being more of a skirmish. And third, the fact that earnings and the economic data continue to look strong.

Yet, at the same time, we should recognize that the bulls aren't showing much "oomph" here. And the fact that a breadth thrust (a period where advancing issues and demand volume overruns decliners, which usually gives the bulls a clear edge for the next 12 months) has yet to occur during this move causes traders to be on the lookout for a sudden end to the market's upside exploration.

So, with new talk about auto tariffs and the trade war with China rapidly expanding to our allies across the pond, it is little wonder that stocks appear to be set for a sloppy open. But so far at least, the bulls have been resilient, and the growth narrative has prevailed.

My fingers are crossed as to whether or not this trend can continue.

Publishing Note: My next report will be published Monday morning.

ANNOUNCEMENT:

HCR Awarded Top Honors in 2018 NAAIM Shark Tank Portfolio Strategy Competition

Each year, NAAIM (National Association of Active Investment Managers) hosts a competition to identify the best actively managed investment strategies. In April, HCR's Dave Moenning took home first place for his flagship risk management strategy.

Want to Learn More? Contact Dave

A Word About Managing Risk in the Stock Market

Thought For The Day:

The foolish and the dead alone never change their opinion. -James Russell Lowell

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

HCR Focuses on a Risk-Managed Approach to Investing

Must Read: What Risk Management Can and Cannot Do

HCR's Financial Advisor Services

HCR's Individual Investor Services

Questions, comments, or ideas? Contact Us

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: None - Note that positions may change at any time.

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.