Reasons For The Rebound

Well that didn't take long! After two days of selling and an awful lot of talk about the end of the economic world as we know it, stocks bounced on Tuesday and are furthering gains in the early going on Wednesday.

So what gives, you ask? Why did we see panic selling one moment and then a spirited rebound the next? From my seat there are a handful of reasons for the schizophrenic behavior in the markets. Cutting to the chase, it appears (a) some reality on the BREXIT front is settling in (b) there is talk of coordinated global central bank intervention, (c) the U.S. economic GDP data wasn't half bad, and (d) technical buying was triggered when the S&P 500 crossed key levels.

Let's start with the sigh of relief. First there was the anti-Brexit rally in Trafalgar Square yesterday. While the rally itself probably wasn't responsible for a bounce in global stocks, the talk regarding the reality of how a BREXIT might work may have. First, traders realized that Friday's vote was not legally binding. It was merely a public referendum on the issue.

In order for the U.K. to actually leave the EU, there would have to be formal notification of the desire to leave given to the EU. And before that happens, apparently the U.K. Parliament needs to vote on the issue.

As such, there was all kinds of talk about how long these moves could take and the obstacles standing in the way of the actual BREXIT such as issues with Scotland and Northern Ireland. Then when you factor in the issue of what is being called a "REGREXIT" and Britain's history of voting more than once on important issues, suddenly the future didn't look so dark.

Central Bankers Mounting Their White Horses

Next comes the idea that the global central bankers of the world are going to do everything in their power to ensure that all of their efforts over the last several years don't go down in flames due to the world's growing distaste for establishment politics.

It started with Super Mario. As I tweeted yesterday morning, ECB President said Tuesday...

You knew it was coming... Draghi: "We can benefit from alignment of policies..."

— Sowell Management (@Sowell_MS) June 28, 2016

Draghi went on to talk about the importance of global central bankers employing coordinated efforts to, in essence, keep things from getting out of hand.

Investors also heard from the Banks of England and Japan. Janet Yellen also weighed in by suggesting that her FOMC governors were watching the situation closely. And then Jerome Powell was the first Federal Reserve policymaker to offer public comment yesterday by saying that the BREXIT vote has shifted global risks "to the downside."

In Fedspeak, such a comment is deemed to mean that the FOMC is worried. Perhaps more importantly, traders recognize that worries over global issues have kept the Fed from raising rates recently and that such worries could keep the Fed on hold for some time going forward.

In short then, part of the upbeat mood in the markets yesterday and today is the fact that traders appear to be expecting the world's central banks to do more to help stimulate the global economy.

A Couple More Things

Oh, and the fact that both GDP and corporate profits during the first quarter here in the good 'ol USofA came in above expectations may have also helped improve the mood.

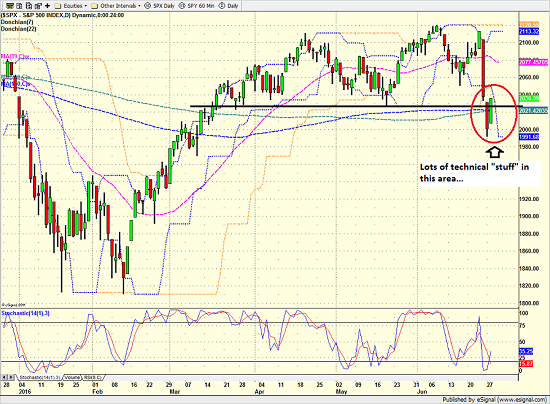

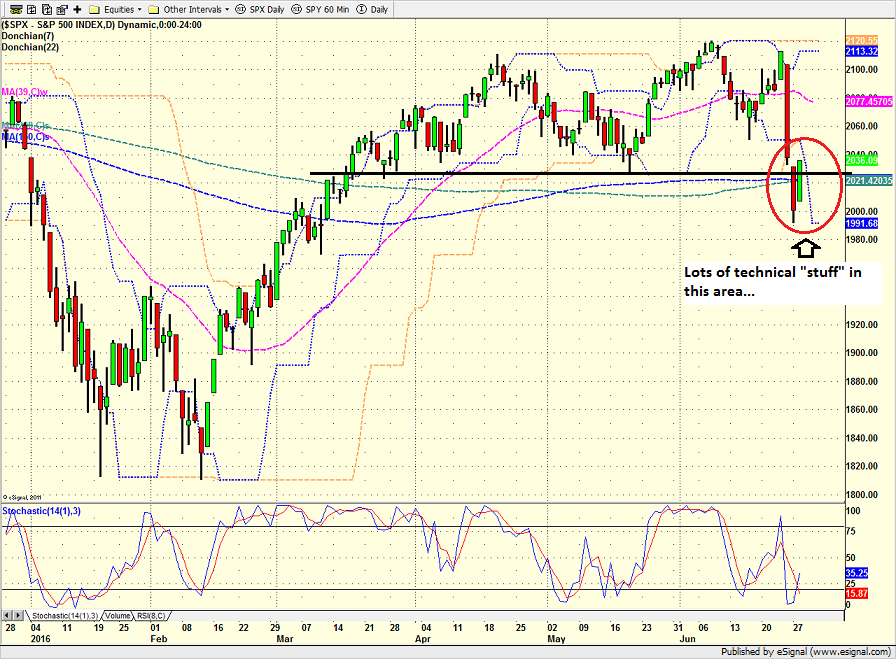

And finally there is the technical picture. Make no mistake about it; for some reason the 150- and/or 200-day moving averages on the major stock market indices remain important to traders. Don't ask me why. But it is important to note that when these key technical levels get crossed - in either direction - trading tends to pick up.

S&P 500 - Daily

View Larger Image

{kind=link}

So there you have it. Two big down days are being followed by a quick rebound. The question of the day, of course, is if the move will morph into a true rebound or merely represent a bounce before the gloom returns.

On the negative side, I will note that the action in the European bank stocks such as Credit Suisse (CS), Deutsche Bank (DB), Barclays (BCS), UBS (UBS) wasn't exactly encouraging. But then again, this is a very fluid situation and today is another day. Thus, we will continue to look at these banks stocks as a potential "tell" for what is to come next.

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The Impact of the "BREXIT"

2. The State of Fed Policy

3. The State of U.S. Economic Growth

4. The State of the Stock Market Valuations

Thought For The Day:

"Always be a first-rate version of yourself, instead of a second-rate version of someone else." - Judy Garland

Here's wishing you green screens and all the best for a great day,

David D. Moenning

Founder: Heritage Capital Research

Chief Investment Officer: Sowell Management Services

Looking for More on the State of the Markets?

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.